Gross Pay vs Net Pay: What’s the Difference? (2026 Plain-English Guide)

⚡ Gross pay vs net pay — quick answer

The difference between gross pay and net pay: gross pay is what you earn before taxes, while net pay is the take-home amount that actually hits your bank account after all deductions.

- Gross pay — your total earnings before any taxes or deductions. The big number on your pay stub. Also called gross wages or gross salary — they all mean the same thing.

- Net pay — what you take home after federal tax, Social Security, Medicare, state tax, and any other deductions are subtracted. Also called take-home pay.

- The difference — the gap between gross and net is all the deductions taken out. For most first-time workers, net pay is roughly 75–85% of gross pay — though it can be higher if only FICA is withheld.

- Which one matters — gross pay for loan applications and salary negotiations. Net pay for your actual budget.

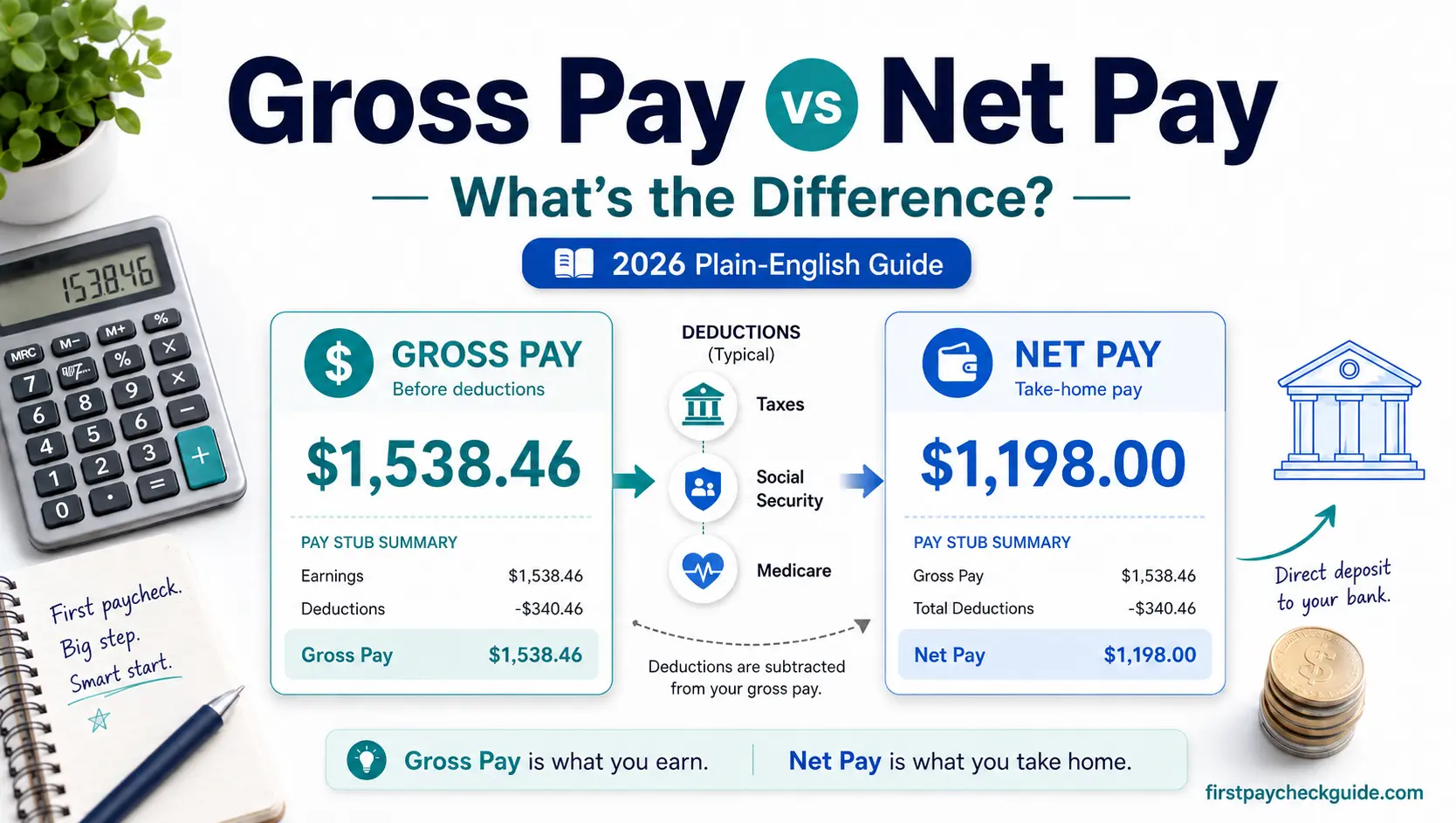

You accepted a job paying $40,000 a year. So why did your first full biweekly paycheck show $1,538 gross — but only $1,198 hit your bank account?

Nothing went wrong. That is the difference between gross pay and net pay — and once you understand it, every paycheck makes sense.

This guide on gross pay vs net pay explains exactly what each one is, what causes the gap between them, and how to calculate both with real 2026 numbers. Whether you are looking at your first pay stub or comparing job offers, this is the reference you need.

Table of Contents

What is gross pay?

Gross pay is the total amount you earn before anything is taken out — it is your starting number on every paycheck. On a pay stub, this is often labeled gross earnings or gross wages. “Gross wages” typically refers to hourly workers. “Gross salary” typically refers to salaried workers. Both reduce to the same gross pay figure that gets taxed and deducted. On your pay stub, gross pay appears at the top as the largest number.

| Worker type | How gross pay is calculated | Example |

|---|---|---|

| Salaried — biweekly | Annual salary ÷ 26 pay periods | $40,000 ÷ 26 = $1,538.46 gross per paycheck |

| Salaried — semi-monthly | Annual salary ÷ 24 pay periods | $40,000 ÷ 24 = $1,666.67 gross per paycheck |

| Hourly — weekly | Hourly rate × hours worked | $15/hr × 40 hrs = $600 gross per week |

| Hourly — biweekly | Hourly rate × hours worked | $15/hr × 80 hrs = $1,200 gross per paycheck |

| Hourly — with overtime | (Regular hours × rate) + (OT hours × rate × 1.5) | $15/hr × 80 hrs + $15 × 1.5 × 8 OT hrs = $1,380 gross |

What is included in gross pay?

Gross pay includes everything your employer pays you before deductions:

- Base salary or hourly wages

- Overtime pay

- Bonuses and commissions

- Shift differentials (extra pay for nights, weekends, holidays)

- Tips reported to your employer

- Allowances (housing, car, meal allowances your employer pays as part of your compensation)

Gross pay vs basic salary — what is the difference?

Basic salary is just your guaranteed base rate — the fixed amount your job pays before overtime, bonuses, or tips. Gross pay is basic salary plus everything else. Basic salary is always the same every pay period. Gross pay can vary depending on hours worked, overtime earned, or bonuses paid.

Example: Your basic salary is $40,000/year. In a pay period where you also earned a $500 bonus, your gross pay for that period is higher than usual. “Gross wages” usually refers to hourly workers. “Gross salary” usually refers to salaried workers. Both show up as gross pay on your pay stub.

What is net pay?

Net pay is what actually lands in your bank account after all deductions are subtracted from your gross pay. It is your real spending money — also called take-home pay.

Several deductions come out before the money reaches your bank account: federal taxes, state taxes, Social Security, Medicare, and anything you signed up for like health insurance or a 401(k). Net pay is what remains.

💡 Is net pay the same as gross pay?

No — net pay is always lower than or equal to gross pay. It can never be higher. For nearly every working American, net pay is meaningfully less than gross pay because at minimum, Social Security and Medicare are always withheld regardless of income level or age.

Is net pay monthly or yearly?

Net pay is per paycheck — not monthly or yearly by default. What you see on your pay stub is your net pay for that specific pay period. If you are paid biweekly, you receive 26 net pay deposits per year. To find your monthly net income, add up the deposits you received in a given month. To find your annual net income, multiply your per-paycheck net pay by the number of pay periods per year.

What if you have no deductions except FICA?

If you are a part-time or young worker who has not signed up for any benefits and earns below the federal withholding threshold — or claimed exempt on your W-4 — your only deductions may be Social Security and Medicare. In that case your net pay is about 92.35% of gross pay since FICA takes 7.65%.

Example: $500 gross pay − $31.00 Social Security − $7.25 Medicare = $461.75 net pay. Nothing is wrong. You just earn too little to owe federal income tax.

Gross pay vs net pay — side by side

| Aspect | Gross Pay | Net Pay |

|---|---|---|

| What it is | Total earnings before deductions | Take-home pay after all deductions |

| Also called | Gross wages, gross income, gross salary, gross earnings | Take-home pay, net wages, net income, net salary |

| Taxes deducted? | No — taxes not yet applied | Yes — all taxes already subtracted |

| Amount | Higher number — always | Lower number — always |

| On your pay stub | Shows at the top as the starting number | Shows at the bottom as the final deposit amount |

| Used for | Loan applications, salary negotiations, tax calculations | Personal budget, rent, actual spending |

| Set by | Your employment contract or hourly rate × hours | Gross pay minus all applicable deductions |

Gross wages vs net pay — is there a difference?

No meaningful difference. Gross wages and gross pay refer to the same thing — your total earnings before any deductions. “Gross wages” is the term payroll systems typically use for hourly workers. “Gross salary” is used for salaried workers. Both get reduced to your net pay (take-home pay) after taxes and deductions are subtracted. On your pay stub, look for “Gross Earnings” or “Gross Wages” at the top. That number minus all deductions equals your net pay at the bottom.

In other words, the difference between gross and net pay is every tax, benefit, and deduction taken out before your paycheck reaches you.

Want to see exactly where gross and net appear on your pay stub? Read: How to Read a Pay Stub →

How deductions reduce gross pay to net pay

The gap between gross and net pay is not random. It is a specific set of deductions applied in a specific order. Here is how your gross pay gets reduced step by step.

- This is your full earnings for the pay period before anything is removed

- For a $40,000/year salaried worker paid biweekly: $1,538.46 gross

- These come out BEFORE taxes are calculated — which means you pay tax on a smaller number, saving you money

- Traditional 401(k) contributions, health insurance premiums, HSA contributions, FSA contributions, commuter benefits

- Example: $100 biweekly to 401(k) + $75 health insurance = $175 pre-tax deductions

- Remaining taxable wages: $1,538.46 − $175 = $1,363.46 taxable income

- Social Security and Medicare are calculated on your Social Security/Medicare wages — which is usually close to gross pay. Traditional 401(k) contributions do not reduce FICA wages, but some cafeteria-plan benefits (health insurance, HSA, FSA) may reduce them slightly depending on your employer’s plan

- Combined FICA rate: 7.65% of Social Security/Medicare wages

- Example: $1,538.46 × 7.65% = $117.69 FICA withheld

- Calculated on your taxable wages — gross minus pre-tax deductions

- Your W-4 settings determine how much is withheld

- For a single filer earning $40,000/year with pre-tax deductions, federal withholding is approximately $80–90 per biweekly paycheck

- 9 states have no income tax on wages: Alaska, Florida, Nevada, New Hampshire, South Dakota, Tennessee, Texas, Washington, Wyoming

- All other states withhold state income tax — rates vary from under 1% to over 10%

- Gross pay minus all deductions equals your net pay

- This is the amount deposited to your bank account or printed on your check

Real examples — gross pay to net pay (2026 figures)

Here is exactly what happens to two different paychecks using real 2026 tax figures.

🧮 Example 1 — $40,000/year salary, biweekly paycheck

Single filer, standard W-4, enrolled in 401(k) and health insurance, state with income tax

| Line item | Amount | Notes |

|---|---|---|

| Gross pay | $1,538.46 | $40,000 ÷ 26 pay periods |

| 401(k) contribution (pre-tax) | − $92.31 | 6% of gross — reduces taxable income |

| Health insurance premium (pre-tax) | − $75.00 | Typical employer-sponsored plan employee share |

| Taxable income after pre-tax deductions | $1,371.15 | This is the number used for federal income tax calculation |

| Social Security (6.2% of gross) | − $95.38 | Applied to gross wages — not reduced taxable income |

| Medicare (1.45% of gross) | − $22.31 | Applied to gross wages |

| Federal income tax (on taxable income) | − ~$80–90 | Single filer, standard W-4, 2026 tables — varies by payroll software |

| State income tax (est. 3%) | − $46.15 | Approximately 3% — varies by state |

| Net pay (take-home) | ~$1,118–1,128 | What lands in your bank account |

On a $40,000 salary with standard benefits, approximately $410–420 per paycheck — about 27% of gross — goes to taxes and deductions. This is why your paycheck is smaller than your salary. Nothing went wrong.

🧮 Example 2 — $15/hour, 80-hour biweekly paycheck

Single filer, standard W-4, no voluntary deductions enrolled yet, state with income tax

| Line item | Amount | Notes |

|---|---|---|

| Gross pay | $1,200.00 | $15 × 80 hours |

| Social Security (6.2%) | − $74.40 | No pre-tax deductions — FICA applied to full gross |

| Medicare (1.45%) | − $17.40 | Applied to gross wages |

| Federal income tax | − ~$55–65 | Single filer, annualized $31,200 — varies by W-4 settings |

| State income tax (est. 3%) | − $36.00 | Approximately 3% — varies by state |

| Net pay (take-home) | ~$1,007–1,017 | Before any voluntary deductions |

At $15/hour with no voluntary deductions, roughly $183–193 per paycheck — about 15–16% of gross — goes to taxes. Adding health insurance or a 401(k) would reduce take-home further but also reduce your taxable income.

Shocked by how small your paycheck was? Read: Why Is My First Paycheck So Low? (7 Real Reasons) →

What if your gross pay changes every paycheck?

If you are hourly, tipped, or paid commission, your gross pay changes every pay period — which means your net pay changes too. Here is what to expect:

Hourly workers with variable hours

More hours means higher gross and higher net — but taxes scale with earnings too. If you work 90 hours instead of your usual 80, your gross goes up by $150 (at $15/hr), but net only goes up by about $120 because taxes take a cut of the extra earnings too.

Tipped workers — the “tiny paycheck” explained

Tips you report to your employer are added to your gross pay and taxed. But FICA and income taxes on those tips get withheld from your small hourly base wages — not from the tips themselves, which you often receive in cash. This is why tipped workers sometimes see very small or even near-zero base paychecks. Nothing is wrong — the taxes on your tips were taken from your hourly wages.

Commission workers

Commissions are added to your gross pay in the period they are earned. A big commission month means a larger tax bill that pay period. Some employers spread withholding evenly — others do not. Check with your payroll team if your withholding looks inconsistent.

The key rule for variable pay

Your net pay is a percentage of your gross pay — not a fixed amount. When gross goes up, net goes up by a smaller percentage because taxes scale. When gross goes down (fewer hours), net drops by a smaller percentage too because some deductions like health insurance are flat amounts. Budget based on your lowest expected paycheck, not your average.

What is FICA? (The deduction everyone asks about)

FICA stands for the Federal Insurance Contributions Act. It is the law that requires both you and your employer to pay into Social Security and Medicare — the programs that give older Americans retirement income and healthcare.

Most W-2 employees pay FICA. There are very narrow exceptions — some student employees working campus jobs while enrolled at least half-time, and certain nonresident alien visa categories — but for 99% of first-time workers, FICA comes out of every paycheck without exception.

| FICA component | Employee rate | Employer rate | What it funds | 2026 wage limit |

|---|---|---|---|---|

| Social Security (retirement, disability, survivors) | 6.2% | 6.2% | Retirement benefits, disability, survivors | $184,500 |

| Medicare (healthcare for 65+) | 1.45% | 1.45% | Healthcare for Americans 65 and older | No limit |

| Combined FICA | 7.65% | 7.65% | Both programs | — |

What happens above the Social Security wage base?

In 2026, Social Security tax stops once your year-to-date earnings exceed $184,500. Medicare tax has no limit — it continues on all wages. High earners also pay an extra 0.9% Additional Medicare Tax on wages above $200,000 for single filers. Most first-time workers will not hit either of these limits, but they explain why higher-income pay stubs look different later in your career.

What does “OASDI” mean on your pay stub?

OASDI stands for Old-Age, Survivors, and Disability Insurance — the official government name for Social Security. If your pay stub says “OASDI” instead of “Social Security,” it is the same 6.2% deduction. Some payroll systems also use “SS Tax” or “Soc Sec.” They all mean the same thing.

Is FICA the same as federal income tax?

No — they are completely separate. FICA is a flat percentage (7.65%) applied to wages to fund Social Security and Medicare. Federal income tax is calculated based on your taxable income, filing status, and W-4 settings — and goes to the general federal budget. Your W-4 only affects federal income tax — not FICA. FICA comes out the same no matter what you put on your W-4.

Your employer pays FICA too

You pay 7.65% and your employer pays 7.65% — so 15.3% total goes to these programs on your behalf. This is why self-employed people pay 15.3% in self-employment tax — they are covering both the employee and employer share themselves.

Official FICA rates

Confirmed at irs.gov/taxtopics/tc751 and Social Security wage base at ssa.gov

Pre-tax deductions — how they reduce both your taxes and your net pay

Pre-tax deductions come out of your gross pay BEFORE federal income tax is calculated. This reduces your taxable income — meaning you pay less in federal income tax. The trade-off is a smaller paycheck, but your tax bill drops too.

| Pre-tax deduction | What it is | 2026 limit | Tax benefit |

|---|---|---|---|

| Traditional 401(k) | Retirement savings through your employer | $24,500/year employee limit | Reduces federal and state taxable income |

| Health insurance premiums | Your share of employer-sponsored health coverage | Varies by plan | Reduces federal and state taxable income |

| HSA (Health Savings Account) | Tax-advantaged medical savings — requires high-deductible health plan | $4,400 individual / $8,750 family | Money goes in tax-free, grows tax-free, and comes out tax-free for medical expenses |

| FSA (Flexible Spending Account) | Medical expenses account — use it or lose it annually | $3,400/year | Reduces federal taxable income |

| Commuter benefits | Transit passes, parking at work | $340/month | Reduces federal taxable income |

How pre-tax deductions actually save you money

If you contribute $200/paycheck to a 401(k) and you are in the 12% tax bracket — which covers most first-time workers earning $40,000 or less — that saves you $24 in federal taxes per paycheck. So the actual cost to your take-home pay is only $176, not $200. As your income grows into higher brackets, the savings increase.

If your employer offers a 401(k) match — say 50% of the first 6% you contribute — you should contribute at least enough to get the full match. It is free money added to your retirement savings on top of your own contribution.

Gross or net pay — which one do you use?

The answer depends on what you are doing. Here is when each one matters:

| Situation | Use gross or net? | Why |

|---|---|---|

| Renting an apartment | Gross pay | Landlords typically require gross income to be 3× monthly rent — they use pre-tax income to assess ability to pay |

| Applying for a loan | Gross pay | Lenders look at your gross pay to calculate debt-to-income ratios and decide if you can afford the loan |

| Personal monthly budget | Net pay | Net pay is your actual spending money — always budget based on what you receive, not what you earn |

| Comparing job offers | Gross first, then estimate net | Job offers and raises are always in gross terms because every person’s taxes and deductions are different. Compare gross salaries first, then estimate take-home. |

| Filing your tax return | Taxable wages from W-2 Box 1 | W-2 Box 1 shows your taxable wages — which is gross pay minus pre-tax deductions, not total gross pay. This is the number that goes on your return. |

| Applying for financial aid or benefits | Gross pay | Most government programs calculate eligibility based on gross income |

Gross pay vs take-home pay — are they different?

Yes. Gross pay is your total earnings before any deductions. Take-home pay is another name for net pay — the amount you actually receive after deductions. They are on opposite ends of the paycheck calculation. Gross pay vs take-home pay and gross pay vs net pay mean exactly the same thing.

Once you know your net pay is the number to budget with, the next question is how to actually divide it. The 50/30/20 rule for your first paycheck breaks that net amount into needs, wants, and savings using real biweekly examples at $15, $18, and $20 an hour, instead of a vague monthly guess.

Net pay YTD — what does it mean?

YTD stands for Year To Date. Net pay YTD on your pay stub shows the total amount you have taken home from January 1 to your most recent paycheck. Gross pay YTD shows your total earnings before deductions for the year. Comparing the two shows exactly how much has been withheld all year — which helps you estimate whether you will get a refund or owe money when you file in April.

The net pay formula

Net Pay = Gross Pay − Pre-Tax Deductions − FICA − Federal Income Tax − State Income Tax − Post-Tax Deductions

In plain English: start with your gross pay, subtract everything that gets taken out, and what is left is your net pay.

| Deduction type | Examples | Reduces taxable income? |

|---|---|---|

| Pre-tax deductions | 401(k), health insurance, HSA, FSA, commuter benefits | ✅ Yes — reduces federal and usually state taxable income |

| FICA taxes | Social Security (6.2%) + Medicare (1.45%) | Usually no for 401(k) — but some Section 125 cafeteria-plan benefits (health insurance, HSA, FSA) may also reduce FICA wages depending on your employer’s plan |

| Federal income tax | Based on W-4 settings and 2026 tax tables — calculated on taxable wages after pre-tax deductions | N/A — this IS the tax |

| State income tax | Varies 0%–13%+ depending on state | N/A — this IS the tax |

| Post-tax deductions | Roth 401(k) contributions, wage garnishments, post-tax life insurance — these come out after all taxes are calculated | ❌ No — taxed before deducted |

How to verify your own gross-to-net calculation

Payroll systems are usually right, but it is still smart to check your first few pay stubs. Here is how to verify the math in about five minutes:

✅ Gross-to-net verification checklist

- Find your gross pay at the top of your pay stub — labeled “Gross Earnings” or “Total Earnings”

- Add up all pre-tax deductions — 401(k), health insurance, HSA, FSA, commuter benefits. Subtract from gross to get taxable wages.

- Check Social Security: multiply your Social Security wages by 6.2%. This is usually close to gross pay, but some pre-tax health or cafeteria-plan benefits may reduce it slightly. The result should be close to your Social Security line on the pay stub.

- Check Medicare: multiply your Medicare wages by 1.45%. Should match your Medicare line. If you earn over $200,000, an extra 0.9% Additional Medicare Tax also applies.

- For federal income tax: use the IRS withholding estimator at irs.gov/W4App to confirm your employer is withholding the right amount

- Add all deductions together. Gross minus that total should equal your net pay. If it is off by more than a few cents, ask HR or payroll to review it.

Frequently Asked Questions

What is the difference between gross pay and net pay?

Gross pay is your total earnings before any taxes or deductions — the big number at the top of your pay stub. Net pay is what you actually take home after all deductions are subtracted: FICA, federal income tax, state income tax, and any voluntary deductions like health insurance or 401(k). Net pay is always lower than gross pay.

What is net vs gross pay in simple terms?

Gross is what you earn. Net is what you keep. If your job pays $40,000 per year, that is your gross salary. After taxes and deductions, you might actually take home around $32,000 — that is your net pay for the year. The gap between the two is everything that gets taken out.

How is net pay different from gross pay?

Gross pay is the full amount you earned before anything is taken out. Net pay is what remains after taxes, FICA, benefits, and other deductions are subtracted. Gross is the starting number on your pay stub. Net is the final deposit in your bank account.

Is net pay higher than gross pay?

No — net pay is always lower than or equal to gross pay, never higher. Gross is what you earned. Net is what remains after deductions. The only scenario where they might be equal is if someone has absolutely no tax liability and no deductions — which is extremely rare in practice.

How do you calculate gross pay?

For salaried workers: divide your annual salary by the number of pay periods per year (26 for biweekly, 24 for semi-monthly, 12 for monthly). For hourly workers: multiply your hourly rate by hours worked that period. Add overtime, bonuses, commissions, or tips earned that period to get your total gross pay.

How do you calculate net pay?

Start with gross pay. Subtract pre-tax deductions (401k, health insurance, HSA) — the result is your taxable income. Then subtract FICA (7.65% of gross wages), federal income tax (based on W-4 and IRS tables), state income tax (varies by state), and any post-tax deductions. What remains is your net pay.

What does FICA mean on my paycheck?

FICA stands for Federal Insurance Contributions Act. It shows up as two separate lines — Social Security (6.2% of gross wages, also labeled OASDI on some pay stubs) and Medicare (1.45% of gross wages). Combined they total 7.65%. These fund your future Social Security retirement benefits and Medicare healthcare. Both you and your employer each pay 7.65%.

Is gross pay the same as take-home pay?

No — they are opposites. Gross pay is before deductions. Take-home pay is another name for net pay — the amount you actually receive after all taxes and deductions. Gross pay is always the larger number. Take-home pay (net pay) is always smaller.

What percentage of gross pay is net pay?

For most first-time workers in 2026, net pay is roughly 75–85% of gross pay depending on your tax situation, state, and benefits enrollment. Someone earning $40,000/year with standard deductions and benefits might take home about 73–77% of gross. A part-time worker with only FICA withheld and no state income tax might take home 92% or more of gross.

Does gross salary include allowances?

Yes. If your employer pays you a car allowance, housing allowance, or meal allowance as part of your compensation, those are included in your gross pay and taxed the same as regular wages. If your base pay is $3,000/month and your employer adds a $500 car allowance, your gross monthly pay is $3,500 and taxes are calculated on the full amount.

Is it better to be paid gross or net?

Job offers and raises are always discussed in gross pay terms because every person’s taxes and deductions are different. There is no option to be paid in net. What you can do is optimize your pre-tax deductions — 401(k), health insurance, HSA — to reduce your taxable income and keep more of your gross pay as take-home without owing more in taxes.

Is net salary monthly or yearly?

Net pay is per paycheck — not monthly or yearly by default. It is calculated fresh for each pay period. To find your monthly net income, add up all deposits received in a given month. To estimate annual net income, multiply your per-paycheck net pay by the number of pay periods per year (26 for biweekly, 24 for semi-monthly, 12 for monthly).

Now You Know the Difference — Read Your Pay Stub

Gross pay and net pay both appear on every pay stub, along with every deduction in between. The guide below decodes every single line on your pay stub in plain English — so you know exactly where every dollar went.

About the Author

Ashief Mahmood is the Founder and Editor of First Paycheck Guide. He researches and explains first-paycheck topics for U.S. first-time workers using IRS publications, U.S. Department of Labor resources, official employer documentation, payroll sources, and carefully labeled estimates.

Ashief is not a financial advisor, tax professional, payroll provider, lawyer, or employer representative. First Paycheck Guide is an independent educational website.

The information in this article is for educational purposes only and does not constitute tax or financial advice. Tax rates, deduction limits, and withholding rules change annually — always verify current figures at irs.gov. FICA rates confirmed via IRS Tax Topic 751. Social Security wage base confirmed via SSA.gov. 2026 401(k) limit ($24,500) from IRS IR-2025-111. 2026 HSA limits ($4,400/$8,750) from IRS Rev. Proc. 2025-19. 2026 FSA limit ($3,400) and commuter benefit ($340/month) from IRS Publication 15-B. Paycheck examples are illustrative and vary by individual tax situation, state, employer, and W-4 settings. Consult a tax professional for guidance specific to your situation.