W-4 vs W-2: What’s the Difference? (Plain-English Guide)

⚡ W-4 vs W-2 — quick answer

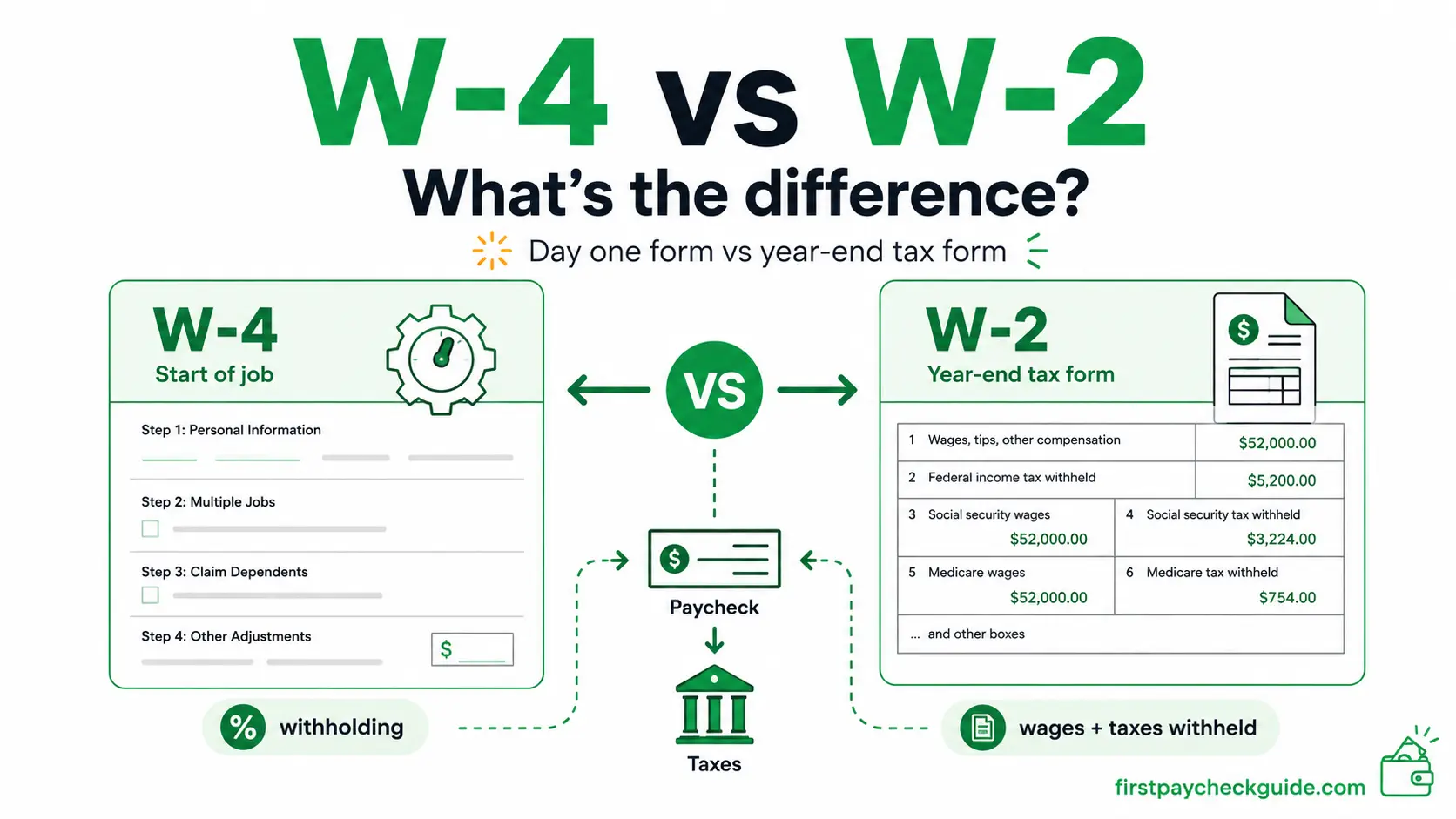

A W-4 tells your employer how much federal tax to withhold from your paychecks; a W-2 reports what you earned and what was withheld for the year. You complete the W-4 when you start a job. Your employer sends the W-2 after the year ends.

- W-4 — filled out by you on day one to set your paycheck tax withholding

- W-2 — prepared by your employer each January to report your annual wages and taxes withheld

- Who fills it out — W-4: you. W-2: your employer.

- Timing — W-4 at job start; W-2 after the year ends

- Connection — your W-4 settings are the main factor that influences the federal tax withheld shown in W-2 Box 2

W-4 vs W-2; what is the difference? If you just started your first job, you have probably seen both forms and still are not completely sure which is which. Here is the plain-English breakdown.

They are related but completely different documents. One is an instruction you give your employer at the start. The other is a record your employer sends you at the end of the year. Understanding the different between W-4 and W-2 takes about five minutes, and it matters because one of them directly controls the size of your paycheck.

Table of Contents

W-4 vs W-2 — the core difference in plain English

Think of it this way: your W-4 is the tax dial you set on your paycheck. Your W-2 is the year-end receipt showing what actually happened.

The W-4 tells your employer how much federal income tax to pull from each paycheck all year. The W-2 tells the IRS, the Social Security Administration, and you how much you earned and how much was withheld over the full year. One tells payroll what to do going forward. The other records what actually happened.

Both W-4 and W-2 forms are for W-2 employees. Contractors usually deal with W-9 and 1099 forms instead.

| W-4 | W-2 | |

|---|---|---|

| Full name | Employee’s Withholding Certificate | Wage and Tax Statement |

| Who fills it out | You — the employee | Your employer |

| Who receives it | Your employer keeps it on file | You receive a copy — the IRS and SSA get one too |

| When | When you start a new job or your situation changes | Generally by January 31 after the tax year ends |

| Purpose | Sets how much federal income tax is withheld from each paycheck | Reports your total wages and total taxes withheld for the year |

| Used for | Payroll — tells your employer how much to deduct each period | Tax filing — you use it to complete your federal and state tax return |

| Sent to IRS? | No — stays with your employer | Yes — your employer files it with the SSA and IRS |

Is a W-2 and W-4 the same thing?

No. They are related but completely different documents serving different purposes at different times of the year. The W-4 is about future withholding — what should come out of your paycheck going forward. The W-2 is about past earnings — what actually came out over the entire year. You fill out a W-4. Your employer fills out a W-2.

What is a W-4 form?

The W-4 is the form you fill out on your first day of work. It has five steps. For most single workers with one job and no dependents, Steps 1 and 5 are all you touch — your name, address, Social Security number, filing status, and signature. Steps 2 through 4 are optional and only apply in specific situations.

What you put on the W-4 directly controls your take-home pay all year. A W-4 that over-withholds gives you smaller paychecks and a bigger refund in April. One that under-withholds gives you larger paychecks but a potential tax bill in April.

| W-4 step | What it covers | Who needs to fill it in |

|---|---|---|

| Step 1 | Name, address, SSN, filing status | Everyone — required |

| Step 2 | Multiple jobs or working spouse | Only if you have 2+ jobs or are married and your spouse also works |

| Step 3 | Dependents and tax credits | Only if you have qualifying children or other dependents |

| Step 4 | Other income, deductions, extra withholding | Optional — most first-timers leave blank |

| Step 5 | Signature | Everyone — required |

For 2026, the child tax credit in Step 3 may be worth up to $2,200 per qualifying child. Use the IRS Tax Withholding Estimator before entering amounts if your situation is not straightforward.

⚠️ The allowances myth — still spreading in 2026

If you find an article telling you to “claim 1 allowance” or “claim 0 allowances” on your W-4 — that article is describing a form that has not existed since 2019. The IRS removed the allowances system entirely when it redesigned the W-4 in 2020. The current form has no allowances section. Any advice that references them is outdated.

Download the official 2026 W-4

Get the current form directly from the IRS: irs.gov/pub/irs-pdf/fw4.pdf

Need to fill out your W-4 right now? Read: How to Fill Out a W-4 for the First Time →

What is a W-2 form?

The W-2 is the document your employer sends you every January showing everything that happened with your pay over the previous year. Your employer — not you — fills it out and delivers it to you. You use it to file your federal and state tax return.

By law, employers must provide W-2s generally by January 31. For tax year 2026, the deadline is February 1, 2027 because January 31, 2027 falls on a Sunday. When the 31st falls on a weekend or holiday, the deadline shifts to the next business day.

Paper vs electronic W-2 — where to find yours

Many employers offer electronic W-2 delivery through payroll portals like ADP, Workday, Gusto, or Paychex. Electronic delivery generally requires your prior consent — if you opted in during onboarding, check your portal in January. If you did not consent to electronic delivery, a paper W-2 should be mailed to your address on file. Not sure which system your employer uses? Ask HR in January — do not wait until April.

| W-2 box | What it shows | Why it matters |

|---|---|---|

| Box 1 | Taxable federal wages | Your taxable income for the year — goes on your tax return |

| Box 2 | Federal income tax withheld | What your employer sent to the IRS from your paychecks all year |

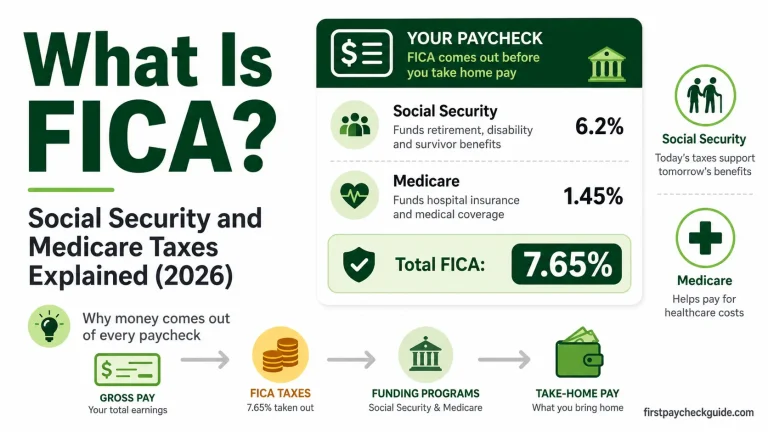

| Boxes 3–6 | Social Security and Medicare wages and taxes | Social Security: 6.2% of Box 3. Medicare: 1.45% of Box 5. These fund FICA. |

| Box 12 | Various codes — 401(k), HSA, life insurance, and new 2026 codes (see below) | Records specific types of compensation and benefits |

| Box 16–17 | State wages and state tax withheld | Used for your state tax return |

New for 2026 W-2s — tips and overtime reporting

Starting with 2026 W-2s, some workers will see new Box 12 codes they have not seen before:

- Code TP — cash tips reported to employer (related to the qualified tips deduction)

- Code TT — qualified overtime compensation (related to the overtime deduction)

- Code TA — employer contributions to Trump Accounts

These 2026 reporting changes are new, so many older W-2 guides may not mention them yet. If you work a tipped or overtime-eligible job, you may see TP or TT on your 2026 W-2. These codes help identify amounts that may qualify for specific deductions on your tax return.

Why W-2 Box 1 may be lower than your gross pay

Box 1 shows taxable federal wages — not your total gross pay. Pre-tax deductions like traditional 401(k) contributions, health insurance premiums, HSA contributions, and commuter benefits reduce Box 1 below your gross pay. This is not an error — it means some of your pay was treated as pre-tax, which lowered your taxable income for the year.

Official W-2 information from the IRS

For full W-2 instructions and requirements: irs.gov/forms-pubs/about-form-w-2

Your W-2 data comes from every pay stub you received all year. Read: How to Read a Pay Stub →

What if your W-2 is missing or has errors?

🚨 W-2 never arrived? Follow these steps in order

- Check your payroll portal (ADP, Workday, Gusto, Paychex) — many employers offer electronic W-2 delivery through these systems

- Check your spam folder for an email from your payroll provider

- Contact HR or payroll to confirm your mailing address and whether your W-2 was sent electronically or by mail

- If still missing after mid-February, call the IRS at 800-829-1040 — they will contact your employer on your behalf

- If you still do not have it by the filing deadline, use Form 4852 as a substitute — it lets you estimate your wages and withholding to file on time

What if your W-2 has errors?

Contact your employer’s payroll or HR department immediately. Common W-2 errors for first-timers include a misspelled name, wrong Social Security number, or incorrect wage amounts. Check all three against your final pay stub of the year.

If an error is confirmed, your employer must issue a corrected W-2 called a W-2c. Do not file your tax return with a W-2 you believe is incorrect — your employer sends a copy to the government too, and the IRS will compare your return against the W-2 on file.

How W-4 vs W-2 work together (the full tax year cycle)

This is the part that makes the forms finally click. The W-4 and W-2 are not just two separate forms — they are cause and effect.

- You hand your employer the W-4 with your filing status and any adjustments

- Your employer enters your W-4 information into their payroll system

- The payroll system calculates how much federal income tax to withhold from every paycheck based on your W-4 settings

- Each paycheck, your employer withholds the amount your W-4 specified

- That withheld money goes to the IRS on your behalf as a prepayment toward what you will owe

- Your pay stub shows the amount withheld each period and the running YTD total

- Your employer totals up everything from all year

- Taxable federal wages → Box 1. Total federal income tax withheld → Box 2

- They file the W-2 with the IRS and SSA, and deliver your copy — generally by January 31 (February 1, 2027 for tax year 2026)

- You use your W-2 to complete your tax return

- Your return calculates what you actually owe based on your income, credits, deductions, and filing status

- Box 2 (what was withheld) vs what you actually owe = your refund or your tax bill

- If your W-4 was set accurately, this difference is small or zero

💡 How W-4 settings influence your W-2

Your W-4 is the main factor that influences Box 2 of your W-2 — the total federal income tax withheld for the year. Higher withholding on your W-4 means a higher Box 2 at year end and a bigger potential refund. Lower withholding means a lower Box 2 and possibly a tax bill in April. The goal is to get Box 2 as close as possible to what you actually owe so you neither overpay throughout the year nor face a surprise bill in April.

When should you update your W-4?

After a big refund or tax bill — update your W-4

A large refund usually means more tax was withheld than necessary during the year. That may feel nice in April, but it also means your paychecks were smaller than they needed to be. Update your W-4 to withhold a little less so that money comes to you throughout the year instead.

A large tax bill means too little was withheld. Update your W-4 immediately to withhold more so it does not happen again next year.

The IRS recommends reviewing your withholding every January and after any major life change. Use the estimator at irs.gov/individuals/tax-withholding-estimator — it takes about five minutes and tells you exactly what to enter on a new W-4.

✅ Update your W-4 when any of these happen

- You start a new job

- You get married or divorced

- You have or adopt a child

- You start a second job or your spouse starts working

- You receive a large tax refund or owe a large tax bill

- Your income changes significantly

- You start freelancing or earning side income

W-4 vs W-2 vs 1099 vs W-9 — what is the difference?

If you have a side hustle or freelance income alongside your regular job, you will encounter two more forms. Here is how all four compare:

| Form | Who it applies to | Who fills it out | What it does |

|---|---|---|---|

| W-4 | W-2 employees at the start of a job | You — the employee | Sets federal income tax withholding from each paycheck |

| W-2 | W-2 employees at year end | Your employer | Reports annual wages and taxes withheld — used to file your tax return |

| 1099-NEC | Freelancers, contractors, gig workers | Client or company that paid you | Reports income paid to you — no taxes were withheld |

| W-9 | Freelancers and contractors before work begins | You — the contractor | Gives your name, address, and SSN to a client so they can send your 1099 at year end |

W-9 in plain English

The W-9 is the contractor equivalent of the W-4. When you start working with a client as a freelancer, they ask you to fill out a W-9 so they have your information on file. At year end they use it to send you a 1099-NEC. You do not send the W-9 to the IRS — it goes to your client only.

| W-2 employee | 1099 contractor | |

|---|---|---|

| Taxes withheld from pay? | Yes — automatically each paycheck | No — you pay them yourself |

| Fill out W-4? | Yes | No — fill out W-9 instead |

| Receive W-2? | Yes — generally by January 31 after year-end | No — receive 1099-NEC instead (also generally by January 31) |

| Self-employment tax? | No — employer pays half of FICA | Yes — 15.3% on net self-employment earnings |

| Can you have both? | Yes — many people have a W-2 job and freelance income. You will receive both a W-2 and a 1099 at tax time and report both on your return. | |

Common W-4 vs W-2 questions

Which form do I fill out when I start a new job?

The W-4. Your employer gives it to you on day one during onboarding. You fill it out and return it to HR. Your employer keeps it on file — you do not send it to the IRS.

When do I get my W-2?

Generally by January 31 in most years. For tax year 2026, the deadline is February 1, 2027 because January 31 falls on a Sunday. Check your payroll portal first — many employers offer electronic W-2 delivery through ADP, Workday, Gusto, or similar systems.

What if I have two jobs — do I need two W-4s?

Yes — one W-4 per employer. Steps 3 and 4(b) should be completed on only one of the W-4s, typically the higher-paying job. Use the IRS estimator at irs.gov/W4App to coordinate withholding accurately across both jobs.

Do I send either form to the IRS?

No to both. Give the W-4 to your employer — they keep it. Your employer sends the W-2 to the IRS and SSA on your behalf. You receive a copy of the W-2 but do not mail it anywhere yourself.

Frequently Asked Questions

What is the difference between a W-4 and W-2?

The W-4 is the form you fill out when you start a job — it tells your employer how much federal income tax to withhold from each paycheck. The W-2 is the form your employer sends you generally by January 31 each year — it shows your total wages and total taxes withheld for the entire year. You use the W-2 to file your tax return. You fill out the W-4. Your employer fills out the W-2.

What is a W-4 vs W-2 in simple terms?

W-4 is the tax dial you set on your paycheck — you give it to your employer at the start of a job to control how much tax comes out each period. W-2 is the year-end receipt — your employer sends it at the end of the year showing what actually happened. One is forward-looking. The other is a record.

Is a W-2 and W-4 the same thing?

No. They are two completely different documents that serve different purposes at different times of the year. The W-4 controls your withholding going forward. The W-2 documents your earnings and withholding after the fact. You complete the W-4 yourself. Your employer completes the W-2.

How does the W-4 affect the W-2?

Directly. Your W-4 settings are the main factor that determines how much federal income tax is taken from each paycheck all year. That cumulative total ends up in Box 2 of your W-2 at year end. Higher withholding on your W-4 means a higher Box 2 and a larger potential refund. Lower withholding means a lower Box 2 and possibly a tax bill in April.

What is the difference between W-4 vs W-2 vs 1099?

W-4 is for employees — you fill it out at the start of a job to set withholding. W-2 is for employees — your employer sends it at year end showing wages and taxes withheld. 1099-NEC is for freelancers and contractors — the company that paid you sends it showing your income with no taxes withheld. If you have both a W-2 job and freelance income, you will receive both a W-2 and a 1099 at tax time.

What is the difference between W-2 vs W-4 vs W-9?

W-4 is for employees — fill it out on day one to set paycheck withholding. W-2 is what your employer sends you at year end showing wages and taxes withheld. W-9 is for contractors — you fill it out for a client before starting work so they can send you a 1099 later. If a company asks for a W-9 instead of a W-4, they are treating you as a contractor, not a W-2 employee.

How many allowances should I claim on my W-4?

None — because the current W-4 does not have an allowances section. The IRS removed allowances when it redesigned the form in 2020. If you are reading advice that says claim 1 or claim 0, that advice is based on a form that no longer exists. The current W-4 uses filing status and dollar amounts instead.

Why is W-2 Box 1 different from my total gross pay?

Box 1 shows taxable federal wages — which is your gross pay minus pre-tax deductions like traditional 401(k) contributions, health insurance premiums, and HSA contributions. These reduce your taxable income, so Box 1 is often lower than your gross pay. This is not an error — it means some of your pay was treated as pre-tax, which lowered your tax bill.

Do I need to fill out a new W-4 every year?

Not unless your situation changes. Your W-4 stays active until you submit a new one. Update it when you get married, divorced, have a child, start a second job, or receive a large refund or tax bill. If you claimed exempt from withholding, you must resubmit a new W-4 every year by February 16 to keep the exemption.

Can I have both a W-2 and a 1099?

Yes — very common. If you have a regular job and freelance income on the side, your employer sends a W-2 for your job income and your clients send 1099-NEC forms for your freelance income. You report both on your tax return. No taxes are withheld from 1099 income — you pay those yourself, typically via quarterly estimated payments.

What’s the difference between a W-4 and a W-2 employee?

A W-4 employee and a W-2 employee are the same thing — a regular employee. The W-4 is the form you fill out when you start the job. The W-2 is the form your employer sends you at year end. Both forms apply to the same person: a standard W-2 employee. If someone is asking whether you are a “W-4 employee or W-2 employee” they are really asking whether you are an employee (W-2) or a contractor (1099).

Does W-4 go with W-2?

Yes — they work together as a pair. You fill out the W-4 at the start of a job to set your tax withholding. Your employer uses those W-4 settings to calculate how much federal income tax to pull from each paycheck all year. At year end, those totals get reported on your W-2. Think of it as the W-4 setting the dial and the W-2 showing the result.

What is a W-4?

The W-4 — officially called the Employee’s Withholding Certificate — is a one-page form you fill out on your first day of work. It tells your employer how much federal income tax to deduct from each paycheck and send to the IRS on your behalf. For most single first-time workers with one job and no dependents, you only need to complete Step 1 (your name, address, SSN, and filing status) and Step 5 (your signature).

Now You Know the Difference — Here Is What to Do Next

Starting a new job? The W-4 is the first form you fill out. Get it right on day one and your withholding will be accurate all year. The guide below walks through every step of the 2026 W-4 with real screenshots from the actual form.

About the Author

Ashief Mahmood is the Founder and Editor of First Paycheck Guide. He researches and explains first-paycheck topics for U.S. first-time workers using IRS publications, U.S. Department of Labor resources, official employer documentation, payroll sources, and carefully labeled estimates.

Ashief is not a financial advisor, tax professional, payroll provider, lawyer, or employer representative. First Paycheck Guide is an independent educational website.

The information in this article is for educational purposes only and does not constitute tax or legal advice. Tax forms, rules, and deadlines change annually — always verify current information at irs.gov. The W-2 delivery deadline for tax year 2026 is February 1, 2027 because January 31, 2027 falls on a Sunday — in most years the deadline is January 31. Self-employment tax rate of 15.3% applies to net self-employment earnings. Consult a tax professional for guidance specific to your situation.