Why Is My First Paycheck So Low? (7 Real Reasons Explained)

⚡ Why is my first paycheck so low? — quick answer

Your first paycheck is usually low because it may cover only part of a pay period, and multiple deductions come out automatically before the money reaches your bank account.

- Partial pay period — you may only be paid for the days worked before payroll closed

- Federal income tax — withheld based on your W-4 and pay frequency (10–22%)

- FICA taxes (Social Security + Medicare) — a fixed 7.65% on every W-2 paycheck

- State and local taxes — 0–9% depending on where you live (Texas/Florida = $0)

- Health insurance and benefits — your share of premiums deducted pre-tax

- 401(k) contributions — if you opted in during onboarding

- Payroll timing — your first check may not include every day you expected

Why is my first paycheck so low? It is the most common question new workers ask; and the answer is almost never “your employer made a mistake.” I still remember staring at my first pay stub at 22, thinking FICA was a typo and seriously considering calling HR.

There are 7 specific, completely normal reasons your take-home pay is smaller than your salary. This guide explains every single one in plain English, plus a checklist to tell if payroll actually did make an error.

Table of Contents

Two terms you need to know first

Gross pay = the number on your offer letter. The fantasy number.

Net pay = what actually hits your bank account. The real number.

Every deduction in this guide takes money from your gross pay before it becomes your net pay. This whole post is about net pay.

Why Is My First Paycheck So Low? Start Here

Yes — almost always. Your first paycheck is typically lower than every paycheck that follows, for reasons that have nothing to do with your employer underpaying you. Here is the short version: your gross pay goes through multiple deductions before it becomes your net pay. On top of that, your first check often covers fewer days than a full pay period.

📊 First paycheck reality check

If your salary is $45,000, your biweekly gross pay is about $1,731. But after FICA, federal withholding, state tax, health insurance, and 401(k), your take-home could easily land around $1,150–$1,350. If your first check covers only half a pay period, it could be closer to $575–$675. You are not bad at money. You are just seeing gross pay, taxes, benefits, and payroll timing collide for the first time.

⚠️ Low paycheck vs delayed paycheck — these are different problems

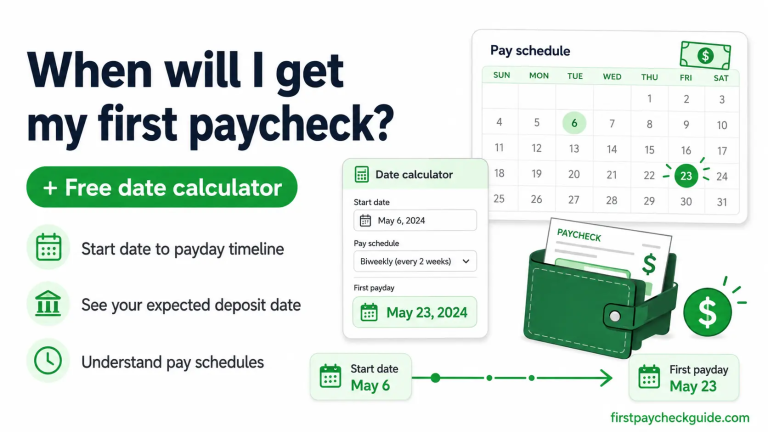

Your first paycheck can be low because it covers only part of a pay period. It can also be delayed because payroll has a fixed cutoff date. If you started after the cutoff, your first days of work may not appear until the following pay period — meaning you could work 2–3 weeks before your first deposit. This is payroll timing, not your employer holding your check.

If you think your check is being held rather than just low, read our guide: Why Do Jobs Hold Your First Paycheck? →

How Much Will My First Paycheck Be After Taxes?

Use this simple formula to estimate your take-home before diving into the 7 reasons:

🧮 First paycheck estimator

Annual salary ÷ pay periods × deduction factor = estimated take-home

Pay periods: Biweekly ÷ 26 · Weekly ÷ 52 · Semi-monthly ÷ 24 · Monthly ÷ 12

Deduction factors: Most states: × 0.72 · Zero income tax state (TX, FL, NV): × 0.78 · High premiums or high-tax state: × 0.68

Examples (biweekly, average state):

$35,000 → $35,000 ÷ 26 × 0.72 = ~$969/check

$45,000 → $45,000 ÷ 26 × 0.72 = ~$1,246/check

$55,000 → $55,000 ÷ 26 × 0.72 = ~$1,523/check

The 0.72 factor assumes roughly 12% federal, 7.65% FICA, 3–5% state, and a few percent for benefits. Adjust using the factors above for your situation.

If your first paycheck is a partial period

Multiply your estimated full paycheck by the fraction of the pay period you actually worked. Worked 7 out of 14 days? Multiply by 0.5. Your next full-period paycheck should be significantly larger.

Reason 1: You Started in the Middle of a Pay Cycle

This is the #1 reason first paychecks look shockingly low — and almost nobody explains it properly. Every employer runs payroll on a fixed schedule with a cutoff date. If your company pays biweekly and their pay period runs from the 1st to the 14th but you started on the 8th — your first paycheck only covers 7 days of work, not 14.

Real calendar example — biweekly pay

Pay period: May 1 – May 14

Your start date: May 8

Days you worked this period: 7 days (May 8–14)

Full period gross pay: $1,538 (on $40k salary)

Your first paycheck gross: ~$769 (half a period)

Your first paycheck net: ~$580–$620 after deductions

Your next full-period paycheck should be closer to the normal $1,538 gross — assuming it covers a complete pay period.

This comes down to where your start date falls relative to the pay period and the payroll cutoff date — the point at which your employer locks hours for that pay run.

Also: most US employers pay in arrears

This means your paycheck pays you for work you already completed during a previous pay period — not for the current week. That is why your first deposit may not arrive right after your first week. The delay is built into the system, not a sign anything is wrong.

How to check if this applies to you

Look at your pay stub — it will show a “Pay Period Start” and “Pay Period End” date. Count the days between your start date and the period end date. If it is less than a full pay period, that is why your check is smaller. Your next paycheck will be significantly larger.

Salary vs Hourly: Why Your Experience Differs

The reasons your first paycheck looks low are slightly different depending on how you are paid:

| Situation | Salaried employee | Hourly employee |

|---|---|---|

| Partial first period | Salary prorated by days worked | Only paid for hours actually clocked |

| Tax withholding basis | Based on annual salary projection | Based on hours × rate × pay periods |

| Hours dispute | Rare — salary is fixed | Common — always verify hours on stub |

| First check surprise | Usually partial period + deductions | Fewer hours than expected + deductions |

⚠️ Hourly workers — always verify your hours

If you are paid hourly, the first thing to check is whether the hours on your pay stub match your own records. Timekeeping errors are the most common payroll mistake for hourly employees. Keep a personal note of your hours every week and compare to your pay stub when it arrives.

$15/hour × 40 hours = $600 gross. After taxes and FICA, your take-home is roughly $480–$520. If it looks significantly lower, check your hours first.

Reason 2: Federal Income Tax Withholding (10–22%)

The US government automatically withholds a portion of every paycheck for federal income taxes. How much depends on your W-4 settings, filing status, and salary. Important: your tax bracket is based on taxable income — not your gross salary. These are rough withholding estimates, not exact rates. See our guide on why no federal income tax was withheld from your paycheck.

| Annual salary | Rough federal withholding per biweekly check | Plain-English note |

|---|---|---|

| $30,000 | ~$55–$65 | Usually modest — standard deduction reduces taxable income significantly |

| $40,000 | ~$90–$105 | Federal tax is lower than most first-timers expect |

| $50,000 | ~$140–$155 | Often still around 12% marginal bracket after standard deduction |

| $60,000 | ~$185–$200 | Withholding rises, but your whole check is NOT taxed at one rate |

⚠️ W-4 over-withholding is extremely common for first-timers

If you left your W-4 on the default settings during onboarding, your employer may be withholding more federal tax than necessary. This gives you a smaller paycheck now and a refund in April — but a refund is not free money, it is money you over-paid the IRS all year.

Check yours using the IRS Tax Withholding Estimator and submit a corrected W-4 to your employer if needed.

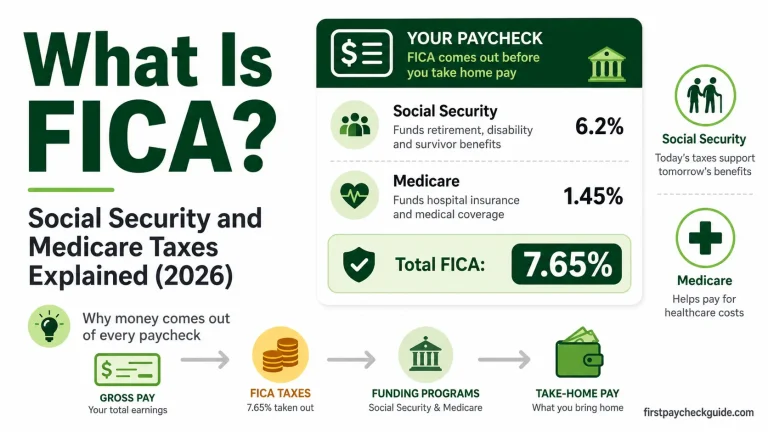

Reason 3: Social Security and Medicare Tax — Called “FICA” (7.65%)

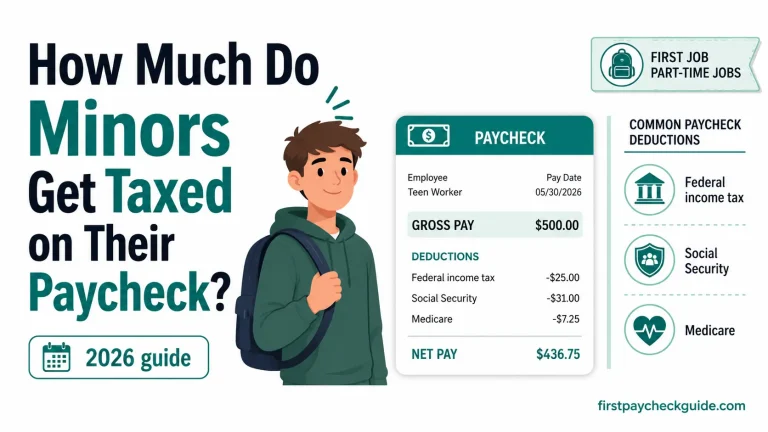

Every W-2 employee pays FICA taxes on every single paycheck — no exceptions. FICA stands for Federal Insurance Contributions Act. It is just the government’s name for Social Security and Medicare combined. For most first-time workers earning under $184,500 in 2026, you pay the full 7.65% on every check.

For a complete dollar breakdown of what taxes come out of a teenager’s paycheck at common hourly wages, read how much minors get taxed on their paycheck.

Reason 4: State and Local Income Tax (0–9%)

Depending on which state you work in, your state government also withholds income tax. And in some cities, there is an additional local tax on top of that.

| State / Location | State income tax rate | Impact on $1,538 paycheck |

|---|---|---|

| Texas, Florida, Nevada, Washington | 0% — no state income tax | $0 deducted |

| Illinois, Michigan | ~4–4.5% | ~$62–$69 deducted |

| New York state | ~6.5% | ~$100 deducted |

| California | ~6% at $40k income | ~$92 deducted (plus SDI) |

Some cities charge local income tax too

A few cities — like New York City, Philadelphia, and some Ohio cities — charge an additional local income tax of 1–4% on top of state tax. Check your pay stub for a separate line labeled “Local Tax,” “City Tax,” or “School District Tax.” If you see one and you do not live in a high-tax city, ask HR to confirm it is correct.

Why is my first paycheck so low in California?

California has both state income tax (~6% at $40k income, rising to ~9.3% above $61k) AND State Disability Insurance (SDI). For 2026 the California SDI rate is 1.3% with no wage limit — this was increased and uncapped starting January 2024. Combined with federal tax and FICA, California employees often take home only 60–70% of gross pay. This is completely normal and not an error.

🌵 Texas and Florida advantage

If you work in Texas, Florida, Nevada, Washington, Wyoming, South Dakota, or Alaska — you pay zero state income tax. That is why workers in these states take home noticeably more than the same salary in California or New York. Use the 0.78 deduction factor in the estimator above instead of 0.72.

Reason 5: Health Insurance and Benefits Deductions

If you enrolled in health insurance, dental, vision, HSA, FSA, or commuter benefits during onboarding, those amounts are deducted from every paycheck. Most are pre-tax deductions — they reduce your taxable income, which is actually good — but they still reduce your take-home pay.

| Benefit deduction | Typical biweekly amount | Pre-tax? |

|---|---|---|

| Health insurance (employee share) | $50–$200 | ✅ Yes — reduces taxable income |

| Dental insurance | $5–$25 | ✅ Yes |

| Vision insurance | $2–$10 | ✅ Yes |

| HSA contribution | $25–$100 | ✅ Yes |

| FSA contribution | $25–$100 | ✅ Yes |

| Commuter benefits (transit/parking) | $25–$100 | ✅ Yes |

| Life insurance (employer-provided) | $5–$20 | Sometimes |

Pre-tax deductions actually save you money

Health insurance comes out before taxes are calculated. If you pay $150 for insurance and you are in the 22% bracket, you save about $33 in taxes per check. Your take-home is lower but your total tax bill is also lower. The deduction is working in your favor even when it does not feel that way.

Tips and commissions note

If you work in food service, retail, or sales and earn tips or commissions, these may appear on a separate pay cycle or be estimated on your first check — which can make the base paycheck look even smaller. Check with your manager or payroll department about how tips and commissions are reported and paid.

Reason 6: 401(k) Contributions

If you opted in to your employer’s 401(k) during onboarding, those contributions are deducted pre-tax from every paycheck. A 4% contribution on a $40,000 salary costs about $61 per biweekly check in take-home pay — but if your employer matches that contribution, you earn an instant 100% return in retirement savings. The smaller paycheck is worth it.

💰 Never skip your 401(k) match

If your employer matches your contributions — say 50% up to 6% of salary — not contributing enough to get the full match is leaving free money on the table. Ask HR: “Do we have a 401(k) match, and how much do I need to contribute to get all of it?” This is the single best financial move you can make in your first week of work.

Reason 7: Your Employer May Have 27 Biweekly Paychecks in 2026

This one is weird and honestly confused me too. Here is the simple version: most years have 26 biweekly pay periods. But depending on when an employer’s payroll calendar falls, some years produce 27 paydays instead of 26. For many biweekly payroll schedules, 2026 is one of those years.

What this means for your paycheck

If your employer divides your annual salary across 27 paychecks instead of 26, each check is slightly smaller. On a $52,000 salary: 27 paychecks = $1,925/check instead of $2,000/check — about $75 less per check.

This does not apply to every employer — it depends on the specific payroll calendar. Ask HR: “Does our company adjust paychecks for a 27-pay-period year?”

Is Your First Paycheck Always Low — or Is Mine Actually Wrong?

Before you contact HR asking why is my first paycheck so low, run through this checklist. Most “low” first paychecks are completely correct — but payroll errors do happen.

✅ Signs your paycheck is LOW but CORRECT

- Your pay period start date is after your actual start date — partial period

- You started after the payroll cutoff date — some days will appear on the next check

- You enrolled in health insurance or other benefits during onboarding

- You opted into 401(k) contributions

- Your state has income tax and you can see it correctly deducted

- FICA taxes are showing at approximately 7.65% of gross

- Your employer is on a 27-paycheck schedule this year

🚨 Signs your paycheck might actually be WRONG — contact HR

- Your pay rate on the stub is different from your offer letter

- Hours worked do not match your own records (hourly employees)

- No taxes are withheld at all — this will cause a large tax bill in April

- Deductions you do not recognize and never agreed to appear

- You are paid as a 1099 contractor but your offer letter says W-2 employee

- Child support or wage garnishment deductions appear that do not apply to you

- A city or local tax is withheld but you do not work in a city with local tax

Copy-paste message to send HR if something looks wrong

Hi [Payroll / HR],

I just received my first paycheck and wanted to confirm a few items. Could you help me verify: the pay period dates, my pay rate, hours worked, tax withholding setup, and benefit deductions? I want to make sure I am reading the pay stub correctly before assuming there is an error.

Thank you.

Payroll corrections are easiest to fix within the same or next pay period — flag it quickly.

Pay Stub Line-by-Line Decoder

Here is what every line on a typical US pay stub actually means — including both pre-tax and post-tax deductions:

Pre-tax deductions (reduce your taxable income):

| Pay stub line | What it means | Typical range |

|---|---|---|

| Gross Pay / Gross Earnings | Your pay before any deductions — the starting number | Salary ÷ pay periods |

| Federal Income Tax (FIT) | Federal tax withheld based on your W-4 and tax bracket | ~10–22% of gross |

| State Income Tax (SIT) | State tax withheld — $0 in TX, FL, NV, WA, WY, SD, AK | 0–9% of gross |

| Local / City Tax | Extra local income tax in some cities (NYC, Philadelphia) | 1–4% if applicable |

| Social Security Tax (OASDI) | OASDI = Old-Age, Survivors, Disability Insurance. Your 6.2% FICA contribution. | Exactly 6.2% |

| Medicare Tax (MED) | Your 1.45% FICA contribution — funds Medicare | Exactly 1.45% |

| Medical / Health Insurance | Your share of employer health plan premium — pre-tax | $50–$200/check |

| Dental / Vision | Your share of dental and vision coverage — pre-tax | $5–$30/check |

| 401(k) / 403(b) Traditional | Pre-tax retirement contribution — lowers taxable income now | 2–6% of gross |

| HSA / FSA | Health savings account — pre-tax, for medical expenses | $25–$100/check |

| Commuter Benefits | Transit or parking deduction — pre-tax in many cases | $25–$100/check |

Post-tax deductions (come out after taxes are calculated):

| Pay stub line | What it means | Normal? |

|---|---|---|

| Roth 401(k) | Retirement contribution taken after taxes — grows tax-free | ✅ Normal if you elected it |

| Union dues | Membership dues if your workplace is unionized | ✅ Normal in union jobs |

| Life insurance (supplemental) | Extra life insurance coverage you elected | ✅ Normal if elected |

| Garnishment | Court-ordered deduction (child support, debt judgment) | 🚨 Only if it applies to you |

| Net Pay / Take-Home Pay | What actually hits your bank account | 65–80% of gross |

For new Walmart associates, the combination of a partial first pay period and FICA deductions can make the first check noticeably smaller than expected. The Walmart first paycheck guide explains exactly what comes out and what a normal first check looks like at $14–$19 an hour.

Learn about the 2026 401(k) limits and how much you should actually contribute at your first job

Want a complete visual guide to every line? Read: How to Read Your Pay Stub for the First Time.

🗓️ Your Payday Action Plan: What to Do in the Next 3 Days

- Pull up your pay stub and find the pay period start and end dates

- Check if your start date falls mid-period — this explains most of the gap

- Verify your pay rate matches your offer letter exactly

- Use the estimator formula above to calculate what your full paycheck should be

- Compare each deduction line against the decoder table above

- If anything looks wrong, send the copy-paste HR message above before the pay period closes

- Check your W-4 at irs.gov/individuals/tax-withholding-estimator

- Confirm your 401(k) contribution rate with HR — make sure you are getting the full employer match

- Set a reminder to check your second paycheck — it should be larger if your first was a partial period

- If you live in California — verify SDI is deducted at 1.3%, not a different rate

Is your first paycheck always low?

Almost always yes — but only the first one. Here is the important distinction most people miss:

📊 First paycheck vs every paycheck after

Your first paycheck is low for two reasons that never repeat: the partial pay period (you started mid-cycle) and the shock of seeing deductions for the first time. Both of these are one-time events.

Your second paycheck will be larger — it covers a full pay period and you are now used to what the deductions look like. From the third paycheck onward everything is consistent and predictable.

So yes — your first paycheck is almost always low. But it is the only one that feels that way.

Frequently Asked Questions

Why is my first paycheck so low?

The most common reasons are: you started mid pay cycle and only got paid for a partial period, taxes and FICA took 20–35% of your gross pay, and benefits deductions reduced it further. This is completely normal. Your next full-period paycheck should be noticeably larger.

Is your first paycheck always low?

Almost always, yes — for two reasons. First, if you started mid pay cycle your first check only covers a partial period. Second, your first paycheck includes all the deductions (taxes, insurance, 401k) that reduce every paycheck going forward. Your second paycheck will feel more normal once you know what to expect.

Is it normal to not get your first paycheck right away?

Yes, completely normal. Payroll runs on fixed cycles with cutoff dates. If you started after the cutoff, your first days of work may not appear until the following pay period — meaning some new employees work 3–4 weeks before their first deposit. This is payroll timing, not your employer holding your check. Most US employers also pay in arrears, meaning you are always paid for work already completed.

Is 2026 a 27-paycheck year?

For many biweekly payroll schedules, yes — 2026 can produce 27 paydays instead of the usual 26. But this depends on your employer’s specific payroll calendar, not a universal rule. If your employer divides your salary across 27 checks, each check is slightly smaller. Ask HR: “Does our company have 27 pay periods in 2026 and does that affect each paycheck amount?”

Why is my first paycheck so low in California?

California workers face multiple deductions that employees in other states do not: state income tax (approximately 6% at $40k, rising to 9.3% above $61k), plus State Disability Insurance (SDI) at 1.3% in 2026 with no wage limit. Combined with federal income tax and FICA, California employees often take home only 60–70% of gross pay. This is normal — not an error.

Why is my first paycheck of the year so low?

January paychecks often look smaller because Social Security taxes reset on January 1. If you hit the Social Security wage base ($184,500 in 2026) late in the prior year, those deductions stopped — then they restart in January. Also, new benefit elections and 401(k) contribution changes typically take effect at the start of the year, which can reduce take-home.

What should I do if my paycheck seems wrong?

First check if you worked a partial pay period — this explains most cases. Then verify your pay rate matches your offer letter and check that hours worked are correct if you are hourly. Use the copy-paste HR message in this article to flag the issue quickly. Payroll corrections are easiest within the same or next pay period.

How much will my first paycheck be after taxes?

A rough estimate: take your annual salary, divide by your number of pay periods (26 for biweekly), then multiply by 0.72 if you live in an average-tax state. Use 0.78 if you live in Texas, Florida, or another zero-income-tax state. Use 0.68 if you have high insurance premiums or live in a high-tax state like California or New York. If your first check covers only part of a pay period, multiply the result by the fraction of days you worked.

Once the shock of a smaller-than-expected check wears off, the next question is usually how to actually divide it. The 50/30/20 rule for your first paycheck breaks that down using real numbers at $15, $18, and $20 an hour, instead of a generic monthly average.

Now You Know Why — Here Is What to Do Next

Your first paycheck is smaller than expected for predictable, completely normal reasons. The partial period resolves itself next check. The deductions are standard. And if something genuinely looks wrong, you now have the checklist and the HR message to fix it fast. The next step: learn exactly how to split what you did receive so you do not run out of money before the next one hits.

The information in this article is for educational purposes only and does not constitute financial or legal advice. Tax rates and deduction rules change annually — always verify current rates at irs.gov, your state’s revenue department, and with your employer’s HR or payroll team.