How to Read a Pay Stub for the First Time (Plain-English Guide)

⚡ How to read a pay stub — quick answer

To read a pay stub, start with the pay period and gross pay, then review taxes, pre-tax deductions, post-tax deductions, and net pay. The goal is to see how your total earnings became the amount deposited in your bank account.

- Header — your name, employer, pay period dates, and pay date

- Gross earnings — total pay before anything is taken out

- Taxes withheld — federal, state, local, Social Security, and Medicare

- Pre-tax deductions — health insurance, traditional 401(k), HSA, or FSA

- Post-tax deductions — Roth 401(k), union dues, garnishments

- Net pay — what actually hits your bank account

Your first pay stub is one of the most confusing documents you will ever receive. It has abbreviations nobody taught you, numbers that do not match your offer letter, and at least one line that makes you wonder if someone made a mistake.

Nobody made a mistake. You just need a translation guide. This post explains how to read a pay stub line by line — every section, every abbreviation, every number — written specifically for people seeing their first pay stub. Think of it as your complete pay stub explained in plain English. No jargon. No assumed knowledge.

Whether you are trying to figure out why your take-home is smaller than your salary, decode what FICA or OASDI means, or just confirm everything looks correct — learning how to read a pay stub is one of the most useful financial skills you can pick up in your first week of work. Let’s go through it together.

Table of Contents

What is a pay stub? (Pay stub meaning explained)

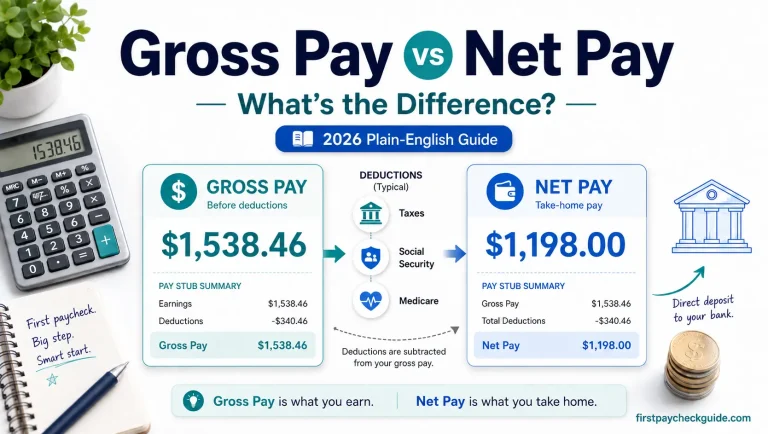

A pay stub — also called a paycheck stub, pay slip, or earnings statement — is a document your employer provides every time you are paid. It shows the complete breakdown of how your gross pay (the total you earned) became your net pay (what landed in your bank account). It is essentially the receipt for your paycheck.

💡 The one sentence that explains everything

Your pay stub is the receipt that shows where the difference between your offer letter salary and your actual bank deposit went — and every single dollar is accounted for on that document.

| Term | What it means | Example |

|---|---|---|

| Pay stub / paycheck stub | The document showing your earnings and deductions | The paper or PDF you get every payday |

| Gross pay | Total earnings before any deductions | $1,538 biweekly on a $40k salary |

| Net pay / take-home pay | What actually hits your bank account | ~$1,066 after all deductions |

| Deductions | Amounts taken from gross pay before you receive it | Taxes, insurance, 401(k) |

| YTD (Year-to-Date) | Running total of earnings/deductions since January 1 | $18,461 YTD gross by month 6 |

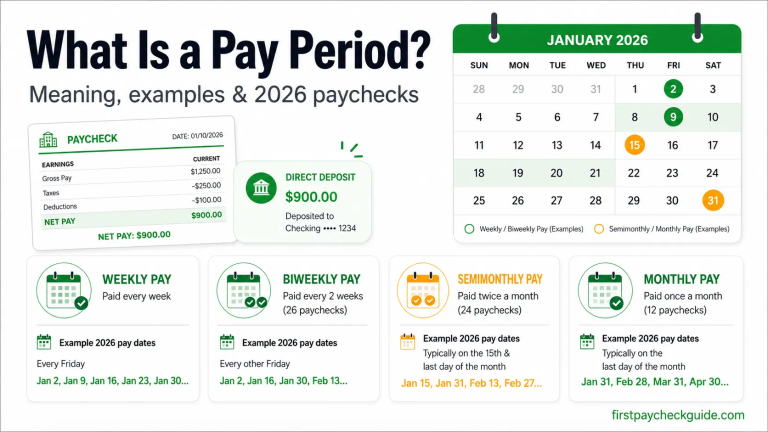

| Pay period | The date range the paycheck covers | May 1–14, 2026 |

| Pay date | The day the money is deposited or check is issued | May 21, 2026 |

Is a pay stub the same as a paycheck?

No. A paycheck is the actual payment — the paper check or direct deposit. A pay stub is the document that explains how that payment was calculated. Many employers now provide only electronic pay stubs via a payroll portal, with no paper check at all. If you are a freelancer or gig worker (1099), you will not receive a pay stub — you will receive a 1099 form instead.

Why does take-home pay look so much lower than your salary? Read: Why Is My First Paycheck So Low? →

Where do I find my pay stub?

Most first-time workers never receive a paper pay stub. Your pay stub almost certainly lives inside your employer’s payroll portal — and nobody tells you this on your first day.

How to access your electronic pay stub — 3 steps

Step 1: Check your work email for an onboarding invite from ADP, Workday, Gusto, Paychex Flex, QuickBooks Workforce, UKG, or Dayforce. Your employer set this up when they added you to payroll.

Step 2: Log in to the portal and look for a tab labeled Pay, Payroll, Payslips, Pay Statements, Earnings, or Documents.

Step 3: Download the PDF for the pay date you want. Save copies of your last 3 months of pay stubs in a secure folder on your phone or computer — you will need them for apartment applications and loan requests.

Paper vs electronic pay stub — does it matter?

For income verification purposes (apartments, loans), a PDF downloaded from your official payroll portal is just as valid as a paper stub. A screenshot is NOT — landlords and lenders can tell the difference. Always download the official PDF and do not alter it in any way.

⚠️ What if I never received a pay stub?

Federal law (FLSA) requires employers to keep accurate payroll records but does not require every employer to hand you a pay stub. Pay stub access is governed by state law. Many states do require pay statements — check your state’s Department of Labor website. If your employer refuses to provide one, ask HR for a written earnings statement. If they still refuse, contact your state’s labor board.

Note: if you started recently and have not been paid yet, your stub does not exist yet. It is generated on or after your first pay date.

Pay stub vs paycheck vs W-2 — what is the difference?

| Document | When you get it | What it shows | What you use it for |

|---|---|---|---|

| Pay stub | Every payday | Current paycheck + YTD running totals | Checking accuracy, income proof for apartments/loans |

| Paycheck | Every payday | The actual payment — paper check or deposit | Spending the money |

| W-2 | By January 31 each year | Annual taxable wages and taxes withheld | Filing your federal and state tax return |

Will my W-2 match my final pay stub YTD numbers?

Not always — and this confuses a lot of first-timers. Your W-2 Box 1 shows taxable federal wages, which may be lower than your gross YTD pay because pre-tax deductions like traditional 401(k), health insurance, and HSA/FSA contributions are subtracted before taxes are calculated. Use your final pay stub of the year to double-check your W-2, but expect some of the numbers to differ for this reason.

How to read a pay stub — section by section

Most US pay stubs follow the same structure regardless of employer or payroll system. Here is every section explained in the order they typically appear.

Section 1: Header information

Always check this section first — errors here can cause tax filing problems down the line.

| What you see | What it means | What to check |

|---|---|---|

| Employee name | Your legal name on file with HR | Must match your ID exactly — spelling errors affect tax records |

| Employee ID / SSN (last 4) | Your employee number or last 4 of Social Security number | Confirm correct with HR if anything looks off |

| Employer name and address | Your company’s legal name and address | Important for income verification and tax filing |

| Pay period | Start and end dates of the work period this check covers | Confirm it matches the days you actually worked |

| Pay date | The day payment is issued — not always the pay period end date | Should match when the deposit hit your account |

| Check number / payment ID | Unique identifier for this specific payment | Reference this if you contact HR about any discrepancy |

First-job note: a few things that confuse new workers

- If your pay period dates do not match your start date — that is normal. You likely started mid-cycle and your first check covers fewer days.

- If your PTO or vacation balance shows 0.00 — that is normal. You have not accrued any yet.

- If there is a voided check image at the bottom of your stub — ignore it. It is just a record-keeping artifact from your direct deposit setup.

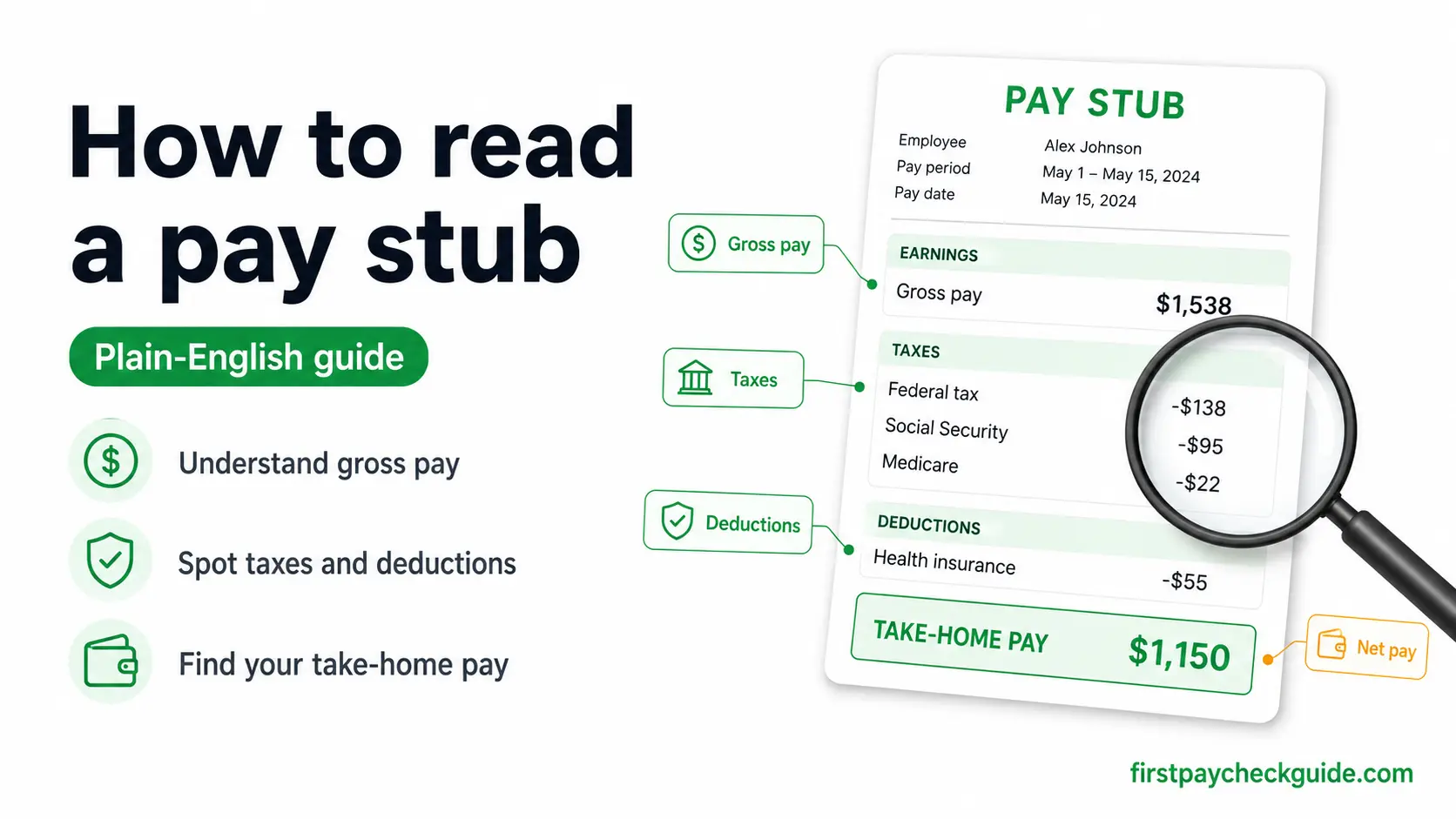

Section 2: Earnings (Gross Pay)

This section shows what you earned before any deductions. This is the starting number — everything else reduces it.

| Line item | What it means | Formula |

|---|---|---|

| Regular pay (REG) | Your base hourly or salary earnings for this period | Hourly: hours × rate | Salaried: annual ÷ pay periods |

| Overtime pay (OT) | Hours over 40/week paid at 1.5× your rate | OT hours × (hourly rate × 1.5) |

| Holiday pay (HOL) | Pay for holidays worked or paid holidays off | Depends on employer policy |

| Bonus / commission (BON/COMM) | Performance pay — may be taxed at higher withholding rate | Varies |

| Tips reported (TIPS) | Tips you reported to your employer for payroll tax purposes | Must report even if paid in cash |

| Gross Pay (total) | Sum of all earnings — the starting number everything else is deducted from | Add all earnings lines above |

Salaried vs hourly gross pay

Salaried: $40,000 ÷ 26 pay periods = $1,538.46 gross per biweekly check — fixed every period.

Hourly: $15/hour × 80 hours = $1,200 gross per biweekly period — varies depending on hours worked.

Section 3: Taxes withheld

This is where most of the “missing money” goes. These are mandatory — your employer is legally required to withhold them and send them to the government on your behalf.

Taxes everyone with a W-2 job pays:

| Pay stub line | What it funds | Rate |

|---|---|---|

| FIT / Federal Income Tax | US federal government | Varies — based on W-4 settings and salary |

| SS Tax / OASDI / Social Security | Social Security retirement and disability benefits | Exactly 6.2% up to $184,500 (2026) |

| Medicare / MED | Medicare healthcare program | Exactly 1.45% on all wages — no limit |

Taxes some people pay (depends on state and city):

| Pay stub line | What it funds | Rate / notes |

|---|---|---|

| SIT / State Income Tax | State government | 0% in TX, FL, NV, WA, WY, SD, AK, TN, NH — up to ~9% in CA/NY |

| Local Tax / City Tax | City or county government | 1–4% in NYC, Philadelphia, some Ohio cities — $0 everywhere else |

| SDI (California only) | California short-term disability fund | 1.3% in 2026, no wage limit |

| SUI EE (some states) | State unemployment fund (employee share) | Very small — varies by state |

What is FICA on a pay stub?

FICA stands for Federal Insurance Contributions Act — the government’s name for Social Security (6.2%) and Medicare (1.45%) combined. Total: 7.65% of your gross pay. You may see FICA as one combined line or two separate lines. Both are correct — it depends on your employer’s payroll software.

What is OASDI on a pay stub?

OASDI stands for Old-Age, Survivors, and Disability Insurance — the formal name for Social Security. Some payroll systems label this line “OASDI” instead of “Social Security Tax.” Same deduction, same 6.2% rate. It stops once you hit $184,500 in wages in a calendar year (2026 limit).

Section 4: Pre-tax deductions

These are benefit contributions taken out before your taxes are calculated. Because they lower your taxable income, they actually reduce your tax bill — even though they reduce your paycheck.

Pre-tax vs post-tax in plain English

Pre-tax means the money comes out before income tax is calculated — so it lowers your tax bill. Post-tax means taxes are calculated first, then the deduction comes out. Both reduce your take-home pay, but only pre-tax deductions reduce your taxable income.

| Pay stub line | What it means | 2026 limit / notes | Typical amount |

|---|---|---|---|

| Medical / Health Insurance | Your share of employer health plan premium | No annual cap on employee share | $50–$200/check |

| Dental | Your share of dental coverage | Pre-tax | $5–$25/check |

| Vision | Your share of vision coverage | Pre-tax | $2–$10/check |

| 401(k) Traditional / 403(b) | Pre-tax retirement savings — taxed when you withdraw in retirement | $24,500 employee limit (2026) | 2–6% of gross |

| HSA | Health Savings Account — triple tax advantage for medical expenses | $4,300 individual / $8,550 family (2026) | $25–$100/check |

| FSA | Flexible Spending Account — for medical or dependent care | $3,300 healthcare FSA (2026) | $25–$100/check |

| Commuter / Transit | Pre-tax transit or parking benefit | $340/month (2026) | $25–$100/check |

| Life Insurance (basic) | Basic employer-provided life insurance premium | Pre-tax if under $50k coverage | $2–$10/check |

Section 5: Post-tax deductions

These come out after taxes are calculated. They do not reduce your taxable income but they do reduce your take-home pay.

| Pay stub line | What it means | Normal? |

|---|---|---|

| Roth 401(k) | Post-tax retirement contribution — withdrawals in retirement are tax-free | ✅ Yes if you elected Roth |

| Union dues | Membership dues if your workplace is unionized | ✅ Yes if union job |

| GTL / Group Term Life | Supplemental life insurance — imputed income if coverage exceeds $50k | ✅ Yes if you enrolled |

| Imputed income (GTL/IMP) | IRS counts employer-paid life insurance over $50k as taxable income you earned — even though you never see the cash. This line just tracks it. | ✅ Normal for high-coverage plans |

| Garnishment (GARN) | Court-ordered deduction for child support or debt judgment | 🚨 Flag if it should not apply to you |

If you are still unsure how to read a pay stub after reviewing these sections, the abbreviations guide below will help.

Section 6: Net pay

Net pay is the final number — the amount that actually hits your bank account. Everything above it was deducted from your gross pay.

🧮 Sample pay stub — $40k salary, biweekly, average state

| Line | Current period | YTD (6 months) |

|---|---|---|

| Gross pay | $1,538.46 | $18,461.52 |

| Federal income tax | -$98.00 | -$1,176.00 |

| Social Security (6.2%) | -$95.38 | -$1,144.57 |

| Medicare (1.45%) | -$22.31 | -$267.69 |

| State income tax | -$65.00 | -$780.00 |

| Health insurance | -$130.00 | -$1,560.00 |

| 401(k) at 4% | -$61.54 | -$738.46 |

| Net pay (take-home) | $1,066.23 | $12,794.80 |

Reading a pay stub — answer key for common first-timer questions

Q: Why does gross pay not match my salary?

Annual salary ÷ pay periods = gross per check. On $40k biweekly: $40,000 ÷ 26 = $1,538.46. If your first check is lower, you started mid pay cycle and only received partial period pay.

Q: Why are there two lines both labeled FICA?

Some stubs show FICA as two separate lines — Social Security (6.2%) and Medicare (1.45%). Others combine them as one FICA line at 7.65%. Both are correct — depends on your employer’s payroll software.

Q: What is the difference between current and YTD columns?

“Current” = this pay period only. “YTD” = running total from January 1. Always use YTD figures when checking annual contribution limits or comparing to your W-2.

Q: Why does my net pay change slightly each period?

Small variations are normal — minor hour changes, PTO payouts, or payroll rounding. Large unexpected drops should be investigated with HR immediately.

Q: What does “EE” mean next to a deduction?

EE = Employee (your share). ER = Employer (their share). “EE Medical” = your health insurance premium. “ER Medical” = what your company pays on your behalf — informational only.

Q: Why is there a line I do not recognize?

Check your benefits enrollment documents first — many first-timers forget they enrolled in optional benefits during onboarding. If it still looks wrong, contact HR with the line description and dollar amount.

What does YTD mean on a pay stub?

YTD stands for Year-to-Date. It is a running total column showing the cumulative amount of each line item from January 1 of the current year through the current pay period.

Why YTD matters for first-time earners

- Use YTD gross pay when an apartment asks for proof of income

- Use YTD federal tax withheld to check if you are over or under-withholding

- Watch your 401(k) YTD contributions — 2026 employee limit is $24,500

- Social Security deductions stop once YTD wages hit $184,500 — most first-timers will never hit this

- Compare your final December pay stub to your W-2 in January — your W-2 Box 1 may be lower than gross YTD due to pre-tax deductions

Pay stub abbreviations — complete guide

Pay stubs use abbreviations to fit everything into a small space. Here is every common abbreviation broken into three groups:

Tax abbreviations:

| Abbreviation | Full name | What it means |

|---|---|---|

| FICA | Federal Insurance Contributions Act | Combined Social Security + Medicare (7.65%) |

| FIT / FWT / FITW | Federal Income Tax (Withheld) | Federal taxes withheld based on your W-4 |

| SIT / SWT / SITW | State Income Tax (Withheld) | State taxes — $0 in TX, FL, NV, WA, WY, SD, AK, TN, NH |

| LIT / CITY / Local | Local Income Tax | City or county tax — NYC, Philadelphia, some OH cities |

| OASDI / SS / SOC SEC | Old-Age, Survivors, and Disability Insurance | Social Security tax — exactly 6.2% |

| MED / Medicare / FED MED | Medicare Tax | Medicare tax — exactly 1.45% |

| SDI | State Disability Insurance | California short-term disability — 1.3% (2026) |

| PFL | Paid Family Leave | California paid family leave deduction |

| SUI / SUI EE | State Unemployment Insurance (employee) | State unemployment fund — very small where applicable |

| Addl Medicare | Additional Medicare Tax | Extra 0.9% for high earners over $200k — most first-timers never see this |

Benefit abbreviations:

| Abbreviation | Full name | What it means |

|---|---|---|

| 401(k) / 403(b) | Retirement Plan | Pre-tax retirement contributions; 403(b) for nonprofits/education |

| HSA | Health Savings Account | Pre-tax medical savings — triple tax advantage |

| FSA | Flexible Spending Account | Pre-tax for medical or dependent care expenses |

| DCAP / DCA | Dependent Care Assistance Program | Pre-tax child/dependent care FSA |

| HRA | Health Reimbursement Arrangement | Employer-funded health expense account |

| GTL / Group Life | Group Term Life Insurance | Life insurance through employer — imputed income if over $50k |

| IMP / IMP INC | Imputed Income | Taxable value of a non-cash benefit (e.g., excess life insurance) |

| LTD | Long-Term Disability | Disability insurance for long-term absence |

| STD | Short-Term Disability | Disability insurance for short-term absence |

| S125 / SEC 125 / CAF | Section 125 Cafeteria Plan | Pre-tax benefits program umbrella term |

| COBRA | COBRA Health Continuation | Health insurance continuation deduction |

| EE | Employee | Your portion of a shared benefit cost |

| ER | Employer | Your employer’s portion — informational, does not reduce your pay |

Earnings and pay type abbreviations:

| Abbreviation | Full name | What it means |

|---|---|---|

| REG | Regular Pay | Standard hours at base rate |

| OT / OVT | Overtime Pay | Hours over 40/week at 1.5× rate |

| HOL | Holiday Pay | Pay for worked or paid holidays |

| BON | Bonus | Performance or signing bonus payment |

| COMM | Commission | Sales-based earnings |

| TIPS | Reported Tips | Tips reported to employer for payroll tax purposes |

| SHIFT / DIFF | Shift Differential | Extra pay for nights, weekends, or special shifts |

| RETRO / ADJ | Retroactive Pay / Adjustment | Back pay or correction for a prior pay period |

| REIMB / EXP | Reimbursement / Expense | Repayment for approved work expenses — not taxable wages |

| PTO / VAC | Paid Time Off / Vacation | Leave hours used or accrued this period |

| VAC ACCR | Vacation Accrued | Vacation hours earned this period |

| SICK / SICK ACCR | Sick Leave / Accrued | Sick time used or earned this period |

| YTD | Year-to-Date | Running total from January 1 to current pay date |

| MTD | Month-to-Date | Running total for the current month |

| QTD | Quarter-to-Date | Running total for the current quarter |

| DD / DIR DEP | Direct Deposit | Payment sent electronically to your bank account |

| GARN / CS / LEVY | Garnishment / Child Support / Tax Levy | Court-ordered or IRS-ordered deductions |

| LOAN | Loan Repayment | Repayment of an employer or retirement plan loan |

| WC | Workers’ Compensation | Usually employer-paid — may appear for informational purposes |

Not every line means money was taken from your paycheck

Some lines are purely informational — employer contributions, PTO balances, accrued sick time, and imputed income tracking. These do not reduce your take-home pay directly. If you see a line and are not sure whether it is a deduction or informational, check whether the amount appears in your net pay calculation or is shown separately without affecting the total.

What counts as a pay stub for apartments, loans, and income proof

| Situation | What they ask for | What counts |

|---|---|---|

| Apartment application | 2–3 most recent pay stubs | Official PDF from payroll portal — paper or electronic both accepted |

| Car loan | Most recent pay stub | Official pay stub showing employer name, gross pay, and net pay |

| Mortgage application | Last 30 days of stubs plus W-2s | Official pay stubs — stubs alone usually not sufficient for mortgage |

| Student loan income verification | Recent pay stub or tax return | Official pay stub is usually accepted |

| Government benefits | Varies by program | Official pay stub — check specific program requirements |

How to get a copy of your pay stub

Log in to your payroll portal (ADP, Workday, Gusto, Paychex Flex, QuickBooks Workforce) and download the PDF. Save at least your last 3 months. If you do not have portal access, ask HR for printed copies. A PDF download from an official payroll portal is accepted everywhere — a screenshot is not.

⚠️ Never use a pay stub generator for income verification

Submitting a fake or altered pay stub for an apartment application, loan, or government benefits is fraud. Most landlords and lenders verify pay stubs against bank statements or by contacting your employer. Always use official pay stubs from your employer’s payroll system.

How to read your paycheck stub for errors — 2-minute review

Payroll errors are common. One EY survey found that 1 in 5 US payrolls contains an error, costing employees an average of $291 each when undetected. Checking your stub every pay period takes 2 minutes and can catch costly mistakes before they compound.

✅ Your 2-minute pay stub review checklist

- Header: name, SSN last 4, pay period dates, and pay date are all correct

- Gross pay matches expected salary ÷ pay periods (or hours × rate for hourly)

- Overtime hours appear at 1.5× if you worked over 40 hours this week

- Federal tax — a reasonable percentage of gross, not zero and not 40%

- Social Security — exactly 6.2% of gross; Medicare — exactly 1.45%

- State tax — matches your state rate ($0 if TX, FL, NV, WA, WY, SD, AK, TN, NH)

- Benefit deductions — match what you enrolled in during onboarding

- No unrecognized deduction lines you never authorized

- Net pay — roughly matches the deposit amount in your bank account

- YTD numbers — increasing each period as expected

Found an error? Copy-paste message to HR

Hi [HR/Payroll Team], I reviewed my pay stub for the period ending [date] and noticed a discrepancy. The [specific line item] shows [amount on stub] but based on my understanding I expected [expected amount]. Could you please review and confirm whether this is correct? Thank you.

📚 What to read next — choose your guide

- If your paycheck arrived but looks smaller than expected → Why Is My First Paycheck So Low?

- If you have not been paid yet and wonder why → Why Do Jobs Hold Your First Paycheck?

- If you understand your stub and want to budget the money → What to Do With Your First Paycheck

Frequently Asked Questions

How do I read a pay stub for the first time?

Start at the top: confirm your name and pay period dates are correct. Then find your gross pay in the earnings section. Then read the deductions — taxes first, then benefits. The final number at the bottom is your net pay, which should match your bank deposit. Use the abbreviations tables in this guide to decode any line you do not recognize.

What is pay stub meaning?

A pay stub is a document your employer provides every payday showing the complete breakdown of your earnings and deductions for that pay period. It shows your gross pay (total earned), all taxes and benefit deductions, and your net pay (take-home amount). It is also called a paycheck stub, payslip, or earnings statement.

What does FICA mean on a pay stub?

FICA stands for Federal Insurance Contributions Act — the combined Social Security tax (6.2%) and Medicare tax (1.45%) that every W-2 employee pays. Together they total 7.65% of gross pay. You may see FICA as one combined line or two separate lines. Both are the same deduction.

What does YTD mean on a pay stub?

YTD stands for Year-to-Date — a running total of each line item from January 1 through your most recent paycheck. Use YTD gross pay to verify your W-2 in January. Note that your W-2 Box 1 may be lower than gross YTD because pre-tax deductions like 401(k) and health insurance reduce your taxable wages.

What does OASDI mean on a pay stub?

OASDI stands for Old-Age, Survivors, and Disability Insurance — the formal government name for Social Security. It appears as either OASDI or Social Security Tax depending on your employer’s payroll system. The rate is 6.2% of wages up to $184,500 in 2026.

What counts as a pay stub for an apartment?

Most landlords accept 2–3 recent official pay stubs showing your employer name, gross pay, net pay, and pay period dates. A PDF downloaded from your employer’s payroll portal (ADP, Workday, Gusto, etc.) is the standard format. A screenshot is not accepted. Landlords typically want stubs from the last 30–60 days.

Why is my pay stub different from my offer letter salary?

Your offer letter states your annual gross salary. Your pay stub shows your actual take-home after taxes and deductions. On a $40k salary paid biweekly, your gross per check is $1,538 — but after federal and state taxes, FICA, health insurance, and 401(k), take-home is typically $1,000–$1,250. This gap is completely normal.

How do I read my pay stub for taxes?

For tax purposes, look at your YTD columns on your last pay stub of the year. Your YTD federal income tax withheld should match W-2 Box 2. Your YTD Social Security wages match W-2 Box 3. Your W-2 Box 1 (taxable wages) may be lower than gross YTD because of pre-tax deductions. If any figures look wrong, contact payroll before filing.

You Can Now Read Any Pay Stub — Here Is What To Do With It

Every line on your pay stub makes sense now. The next step is making sure the money that reaches your bank account is working as hard as possible for you. Start with the step-by-step action plan in our first paycheck guide.

The information in this article is for educational purposes only and does not constitute financial, tax, or legal advice. Tax rates, contribution limits, and payroll rules change annually — always verify current rates at irs.gov, ssa.gov, and your state revenue department. For 2026: Social Security wage base $184,500 (SSA.gov); employee Social Security tax rate 6.2%; Medicare tax rate 1.45%; 401(k) employee elective deferral limit $24,500 (IRS Notice 2025-67); qualified transportation fringe benefit monthly exclusion $340 (IRS Publication 15-B 2026); California SDI rate 1.3% with no wage limit (California EDD).