What to Do With Your First Paycheck: A Step-by-Step Guide (2026)

⚡ What to Do With Your First Paycheck — A Step-by-Step Plan

- Expect it to be smaller — taxes and deductions take 25–35% of your gross salary

- Calculate your real take-home pay — budget from your net pay, not your salary offer

- Pay bills due before your next paycheck — rent, utilities, groceries, minimums first

- Move 10–20% to savings immediately — before you spend on anything else

- Get your full 401(k) match — if your employer offers one, this is free money

- Budget one small treat — $20–$50 to celebrate, decided in advance

- Automate everything — direct deposit split, auto-transfers, budgeting app

You worked hard, waited two weeks, and finally — your first paycheck landed. Then you looked at the number and thought: wait, that’s it?

If you are wondering what to do with your first paycheck and your first reaction was confusion, mild panic, or the feeling that someone made a mistake — you are not alone. Almost every first-time earner goes through the exact same moment. I still remember staring at my first pay stub at 22, trying to figure out if FICA was a typo.

This guide will do two things: first, explain why your paycheck looks smaller than expected. Then walk you through exactly what to do with it — step by step, with real dollar examples — so you start your financial life on the right foot.

Table of Contents

When Will You Actually Get Your First Paycheck?

Before you can budget money, you need to know when it is coming. Most US employers run payroll on one of four schedules:

Why Your First Paycheck Might Be Delayed

Payroll systems run on cut-off schedules. If you started mid-cycle, your first two weeks of work may not process until the following pay period — meaning you could work 3–4 weeks before seeing your first deposit. This is normal and legal in most states. It is payroll lag, not your employer holding your check.

Ask HR on day one: “When is the next payroll cut-off date, and when will I see my first direct deposit?”

If your first check is smaller than expected or arrives later than you thought, the payroll cutoff date is usually the reason — the deadline your employer uses to lock hours before processing pay.

If your first deposit just came from Walmart, the Walmart first paycheck guide has the full breakdown of what came out of your check and what a realistic budget looks like on a Walmart bi-weekly schedule.

Worried your check is being held? Read: Why Do Jobs Hold Your First Paycheck? → Not sure when your first deposit arrives? Read: When Will I Get My First Paycheck? →Why Your First Paycheck Is Smaller Than You Expected

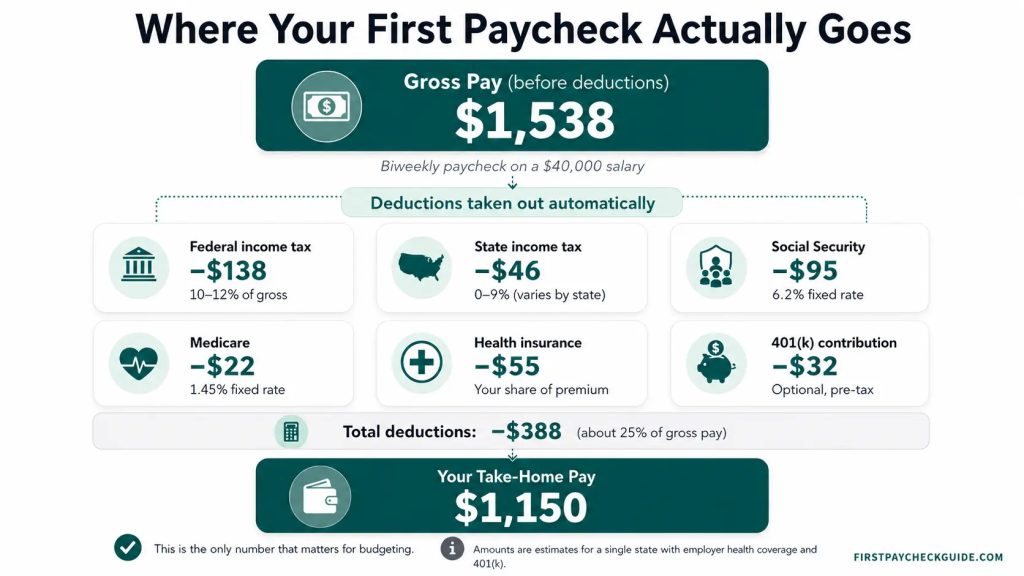

If you were offered a $40,000 annual salary, here is what your gross pay actually looks like per paycheck — before any deductions:

| Pay Schedule | Gross Pay Per Check | Typical Take-Home (after tax) |

|---|---|---|

| Monthly | $3,333 | ~$2,500–$2,700 |

| Semi-monthly (2×/month) | $1,667 | ~$1,250–$1,350 |

| Biweekly (every 2 weeks) | $1,538 | ~$1,100–$1,250 |

| Weekly | $769 | ~$580–$630 |

Here is what gets taken out of every paycheck before it reaches you:

💡 The Number That Actually Matters

After all deductions, most first-time earners take home 65–80% of gross pay. That final deposit amount — your net pay or take-home pay — is the only number that matters for budgeting. Not your salary. Not your offer letter. This number.

A Note on Your W-4 Form

On your first day, you filled out a form called the W-4 — this tells your employer how much federal income tax to withhold from each paycheck. Filling it out incorrectly is very common and can mean you owe money in April (under-withheld) or gave the IRS an interest-free loan all year (over-withheld).

Check yours using the IRS Tax Withholding Estimator at irs.gov. You can submit a new W-4 to your employer any time.

✅ Before You Spend: Quick Pay Stub Checklist

- Your name and address are correct

- Your pay rate or salary matches your offer letter

- Hours worked are correct (critical if you are hourly)

- Tax deductions look reasonable — not zero, not 50%

- Direct deposit went to the right bank account

Want to understand every line on your pay stub? Read: How to Read Your Pay Stub for the First Time →

Step 1: Calculate Your Actual Take-Home Pay

Before you spend a dollar, find your real monthly income using this simple formula:

🧮 Monthly Take-Home Formula

Net paycheck × 26 ÷ 12 = monthly take-home pay

Example: $950 × 26 = $24,700 ÷ 12 = $2,058/month

💡 Tip: Two months per year you’ll get a 3rd biweekly paycheck — use that for savings or debt payoff.

Step 2: Pay the Bills Due Before Your Next Paycheck

Your first paycheck has one job before anything else: keep your life running until the next one arrives. List every bill due in the next two weeks and cover those first.

| Essential Expense | Example Amount | Priority |

|---|---|---|

| Rent / share of rent with roommate | $500–$900 | 🔴 Must pay |

| Utilities (electricity, internet, gas) | $60–$120 | 🔴 Must pay |

| Groceries | $100–$180 | 🔴 Must pay |

| Transportation (gas, transit pass) | $60–$150 | 🔴 Must pay |

| Student loan minimum payment | $80–$200 | 🟡 Pay minimum |

| Credit card minimum | $25–$80 | 🟡 Pay minimum |

| Everything else | What’s left | Now you budget |

Still Living With Your Parents?

Your essentials might be as low as $150–$300 per paycheck instead of $700+. That means you can save 40–50% right from day one — a genuine financial head start. Use it aggressively.

Not sure how much rent you can afford? Read: How Much Rent Can I Afford on My Salary? →

Step 3: Save Before You Spend — And Get Your 401(k) Match

Here is the one habit that separates people who build wealth from people who wonder where their money went: save first, spend what is left. Move money to savings the moment your paycheck arrives — before anything else hits your account.

| Take-Home Per Paycheck | Save 10% | Save 20% |

|---|---|---|

| $750 | $75 | $150 |

| $950 | $95 | $190 |

| $1,200 | $120 | $240 |

| $1,500 | $150 | $300 |

💰 The 401(k) Match — Don’t Skip This

If your employer matches 401(k) contributions, this is the single best financial move you can make in your first week. If they match 50% up to 6% of your salary, contributing 6% gives you an instant 50% return — better than any savings account on earth. Ask HR: “Do we have a 401(k) match, and how much do I need to contribute to get all of it?”

Your First Savings Goal: The Starter Emergency Fund

Before anything else, build a separate savings account with $500–$1,000 that you do not touch unless something unexpected happens. Think of it as “enough to fix your car without a panic attack.” Once you hit $1,000, your longer-term goal is 3–6 months of essential expenses.

Learn more: What Is an Emergency Fund and How to Start One →

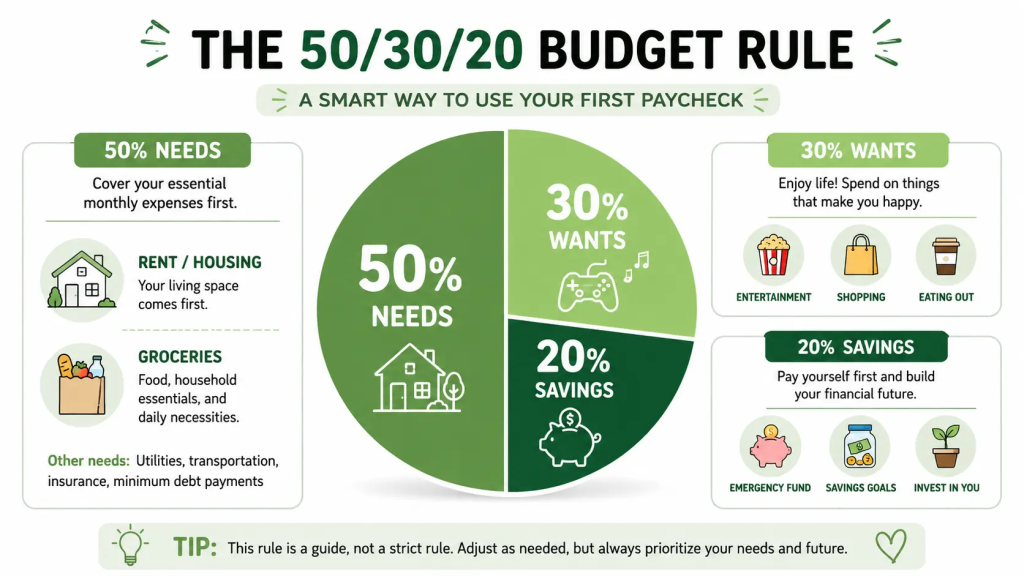

Step 4: Use the 50/30/20 Rule as Your Budget Target

Understanding what to do with your first paycheck means having a system for every dollar — and the 50/30/20 rule is the simplest framework for beginners.

The 50/30/20 rule is your overall budget framework. Think of it as a money diet — but one where you are allowed to eat the cake if it fits the plan. “Pay yourself first” (Step 3) is simply the method for hitting the 20% savings target automatically before the wants category eats it.

| Bucket | % of Take-Home | What Goes Here | On $2,000/month |

|---|---|---|---|

| 🔴 Needs | 50% | Rent, food, transport, utilities, debt minimums | $1,000 |

| 🟡 Wants | 30% | Eating out, subscriptions, fun, clothes | $600 |

| 🟢 Savings | 20% | Emergency fund, 401(k), extra debt payoff | $400 |

⚠️ If You Live in NYC, SF, or Another High-Cost City

Your “needs” may eat 60–65% of income. That is okay — adjust the percentages to fit your reality. The one rule that does not bend: savings is never zero. Even $50 per paycheck builds the habit.

Deep dive: The 50/30/20 Rule Explained for Your First Job →

Not sure what a pay period is or when you get paid? Read: What Is a Pay Period? →Step 5: Give Yourself a Small Reward

Yes, Really — You Earned This

Getting your first paycheck is a genuine milestone. The treat could be a nice dinner, that video game you have been putting off, or yes — DoorDash, no cooking required. We are not saying make a five-course meal to celebrate.

The key word is fixed. Decide the exact amount before you spend — $20, $50, whatever fits — and that is the ceiling. A budgeted reward gives you permission to enjoy your money without torching your plan. Think of this step as the antidote to “I got paid and somehow I’m broke three days later.”

Step 6: Automate Your Budget So You Don’t Have to Think About It

Direct Deposit Splitting — The Most Underused Money Trick

Most US employers let you split your direct deposit between two accounts — for example, 80% to checking and 20% directly to savings. The money never hits your checking account so you never see it and never spend it. Ask HR or your payroll portal about this on day one. It is the single most effective saving method available and almost nobody uses it.

Best free budgeting apps in 2026:

| App | Cost | Best For |

|---|---|---|

| Rocket Money | Free tier available | Tracking subscriptions and spending |

| Monarch Money | Free trial, then paid | Clean interface, full budget view |

| Goodbudget | Free version available | Envelope-style budgeting for beginners |

| Your bank’s app | Free | Quick spending breakdowns, zero setup |

| Google Sheets | Free | Full control, totally customizable |

Full comparison: Best Free Budgeting Apps for First-Time Earners →

Common First Paycheck Mistakes to Avoid

⚠️ Watch Out for These

- Budgeting from your gross salary, not net pay. Your take-home is the only number that matters.

- Waiting until month-end to save. There will never be money left. Save on payday, not after.

- Skipping your 401(k) match. Not contributing enough to get the full match is leaving free money uncollected.

- Lifestyle inflation on day one. Don’t trade your reliable car for a lease payment the day you get your offer letter. Give yourself 60–90 days to see your real numbers first.

- Using Buy Now Pay Later (BNPL) to treat yourself. Klarna and Afterpay are future bills you haven’t earned yet. Your celebration should come from your actual paycheck.

- Celebrating a big tax refund. A large refund means you over-withheld and gave the IRS an interest-free loan all year. Check your W-4 now.

- Forgetting your subscriptions exist. You probably have $40+ in services quietly charging your account every month. Check your bank statement right now.

How to Split Your First Paycheck — Real Examples

Most articles give you monthly examples. Here is how to actually split a single paycheck — the moment it hits your account.

Example A — $950 Paycheck

Hourly / entry-level first job

| Bills due before next payday | $450 |

| Groceries and transport | $150 |

| Starter emergency fund | $100 |

| Student loan minimum | $75 |

| Budgeted treat 🎉 | $50 |

| Buffer until next paycheck | $125 |

| Total | $950 |

Example B — $1,400 Paycheck

Salaried / first full-time job

| Rent and utilities (share) | $650 |

| Groceries and transport | $150 |

| Emergency fund savings | $150 |

| Student loan minimum | $120 |

| 401(k) to get full match | $80 |

| Budgeted treat 🎉 | $75 |

| Buffer | $175 |

| Total | $1,400 |

📊 The Honest Truth

Most people wing it and regret it by day 10. You just ran the actual numbers for your paycheck. That puts you ahead of 90% of first-time earners who never do this exercise at all.

🗓️ Your First Paycheck — 7-Day Action Plan

- Calculate your monthly take-home pay using the formula above

- List all essential bills due before your next paycheck

- Open a separate savings account if you do not have one

- Ask HR about direct deposit splitting — set it up immediately if available

- Ask HR about your 401(k) match — contribute enough to get the full match

- Download one budgeting app and connect your bank account

- Set up an automatic savings transfer on payday as backup

- Decide your treat amount and spend it with zero guilt

- Check your W-4 using the IRS Tax Withholding Estimator at irs.gov

- Verify your pay stub against the 5-point checklist above

- Set a calendar reminder to review your spending in 30 days

- Bookmark your budget and check it once a week going forward

Frequently Asked Questions

How much should I save from my first paycheck?

One of the most common questions about what to do with your first paycheck is how much to save. Aim for at least 10% of your take-home pay. If that is not possible right now, start with $25–$50 — the habit matters more than the amount. Automate it so it happens without you having to decide every payday.

My first paycheck was way smaller than I expected — is that normal?

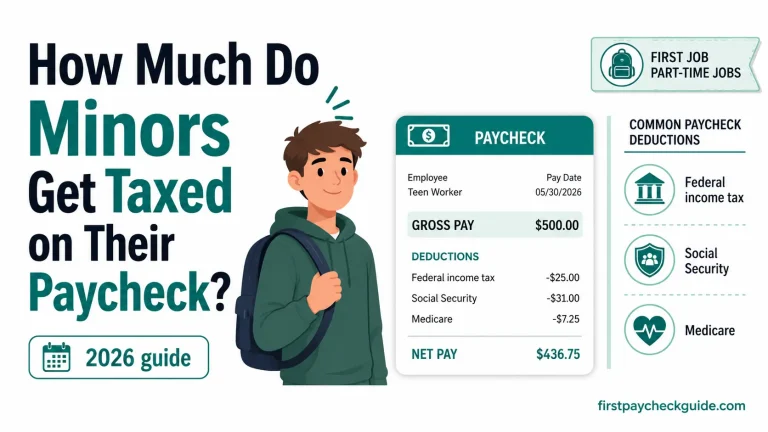

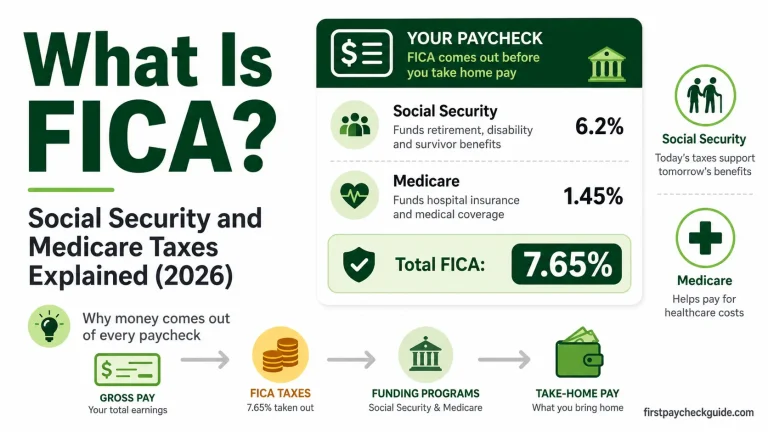

Completely normal. Federal and state income taxes, Social Security (6.2%), Medicare (1.45%), and benefit deductions can reduce gross pay by 20–35%. Your net pay — what actually lands in your account — is the only number you budget from.

Why is my first paycheck delayed?

Payroll runs on fixed cut-off schedules. If you started mid-cycle, your first two weeks may not process until the following pay period. Ask HR when the next payroll cut-off is so you know exactly what to expect and when.

Should I pay off debt or save with my first paycheck?

Do both in this order: first, get your employer’s full 401(k) match. Second, build a $500–$1,000 starter emergency fund. Third, make minimum payments on all debts. Fourth, direct extra money toward your highest-interest debt first.

What if my first paycheck is from DoorDash, Uber, or a gig platform?

Gig platforms pay you as a 1099 contractor — zero taxes are withheld. That is not free money. You owe self-employment tax (15.3%) plus income tax. Set aside 25–30% of every gig payment for taxes and look into quarterly estimated payments to avoid an April penalty.

Can I spend some of my first paycheck on something fun?

Absolutely — and you should. Budget a fixed amount before you spend it, not after. A planned treat is part of a healthy financial life. Unplanned spending is what derails everything by day three.

How do I set up direct deposit for my first paycheck?

Ask HR for a direct deposit form on your first day. You will need your bank’s routing number (9 digits, on the bottom left of a check), your account number, and your account type (checking or savings). Most payroll portals let you add this online through the employee portal.

You Just Got a Head Start on Your Financial Life

Your first paycheck is smaller than your salary — and now you know exactly why and what to do about it. Cover your essentials, save before you spend, get your 401(k) match, and set up systems that run automatically. You do not need to be perfect. You just need to start with a plan — and you just did.

Read Next: Why Is My First Paycheck So Low? (7 Real Reasons Explained) →The information in this article is for educational purposes only and does not constitute financial advice. Please consult a qualified financial professional for advice specific to your situation.