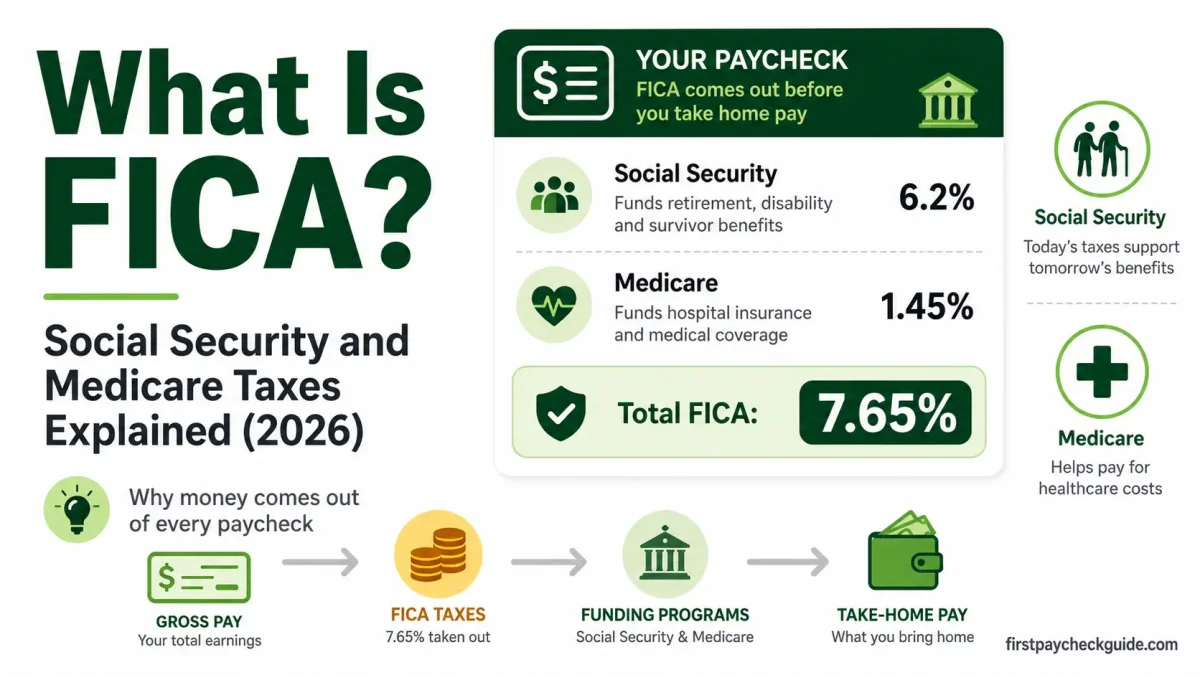

What Is FICA? Social Security and Medicare Taxes Explained (2026)

⚡ What is FICA — quick answer

FICA is a mandatory federal payroll tax that takes 7.65% from every paycheck — 6.2% for Social Security and 1.45% for Medicare. Your employer pays another 7.65% on top of that. FICA stands for Federal Insurance Contributions Act.

- Social Security — 6.2% of your gross wages, up to $184,500 in 2026. Funds retirement, disability, and survivors benefits.

- Medicare — 1.45% of your gross wages with no income limit. Funds healthcare for Americans 65 and older.

- Combined rate — 7.65% total comes out of your paycheck every time, no exceptions.

- Do you get it back? — No. FICA is not a withholding — it is a tax. Think of federal income tax as money you lend the government. FICA is money you invest in your future safety net.

You just got your first paycheck. You did the math in your head; $15 an hour x 40 hours = $600. But your actual check is closer to $520. Where did the other $80 go?

The biggest culprit is a line item called FICA. It is not a typo. Is is not a mistake by your employer. And no, you cannot ask your boss to remove it.

Here is exactly what FICA is, why it takes 7.65% of your paycheck, and what you get in return- explained in plain English for your first job.

Table of Contents

What does FICA stand for?

FICA stands for the Federal Insurance Contributions Act — a federal law from 1935 that requires employees and employers to contribute to two programs: Social Security and Medicare. Think of it like a forced savings account for your future self. You cannot opt out, but you do get benefits from it later in life.

Every time you earn a paycheck, a fixed percentage goes into these two federal programs that provide financial support to older Americans, people with disabilities, and survivors of deceased workers. You pay in now. You benefit later.

Why do I see “OASDI” on my pay stub instead of FICA?

OASDI stands for Old-Age, Survivors, and Disability Insurance — the official government name for Social Security. Some payroll systems label it OASDI, others use “Soc Sec” or “SS Tax.” They all mean the same thing: the 6.2% Social Security portion of your FICA deduction. Medicare sometimes appears as “MED” or “HI” (Hospital Insurance). All of these are FICA.

📋 FICA pay stub decoder — what every label means

Your pay stub may use any of these labels for FICA. They all refer to the same deductions:

| Pay stub label | What it means | Rate |

|---|---|---|

| OASDI | Social Security tax (Old-Age, Survivors, and Disability Insurance) | 6.2% |

| Soc Sec | Social Security tax | 6.2% |

| SS Tax | Social Security tax | 6.2% |

| Medicare | Medicare tax | 1.45% |

| MED | Medicare tax | 1.45% |

| HI | Hospital Insurance — the Medicare portion | 1.45% |

How much does FICA take from your paycheck?

FICA is two separate taxes calculated differently. Here is how each one works:

Social Security — 6.2%

Your employer withholds 6.2% of your gross wages for Social Security. In 2026, this applies to the first $184,500 you earn in a year — called the wage base. Anything above that amount is not subject to Social Security tax for the rest of the year.

| Your gross pay per check | Social Security withheld (6.2%) | Medicare withheld (1.45%) | Total FICA per check |

|---|---|---|---|

| $400 (weekly, $10/hr) | $24.80 | $5.80 | $30.60 |

| $600 (biweekly, $15/hr part-time) | $37.20 | $8.70 | $45.90 |

| $1,200 (biweekly, $15/hr full-time) | $74.40 | $17.40 | $91.80 |

| $1,538 (biweekly, $40k salary) | $95.38 | $22.31 | $117.69 |

Medicare — 1.45%

Medicare takes 1.45% of your gross wages every paycheck. Unlike Social Security, Medicare has no wage base limit — it applies to every dollar you earn regardless of how much you make.

Total FICA — 7.65%

Add them together and you get 7.65%. On that $600 gross paycheck, FICA takes $45.90 before anything else comes out.

Do tips count for FICA?

Yes — if you work in a restaurant, café, delivery, or any tipped job, FICA applies to your reported tips too, not just your hourly wage. If you report $200 in tips in a pay period, that $200 is subject to the same 7.65% FICA as your regular wages. This is one reason take-home pay in tipped jobs can feel lower than expected even in a good week.

The Additional Medicare Tax — 0.9% above $200,000

High earners pay an extra 0.9% Medicare tax on wages above $200,000 for single filers ($250,000 married filing jointly, $125,000 married filing separately). This is unlikely to affect your first job, but it explains why the FICA deduction looks slightly different on high-income pay stubs and why the calculator shows it for higher salary inputs.

Does my employer pay FICA too?

Yes — and most first-time workers have no idea about this. Your employer pays the exact same amount you do.

💡 The full FICA picture

You pay 7.65% of your wages. Your employer pays another 7.65% on top of that. The total FICA contribution on your earnings is actually 15.3% — but you only see your half on your pay stub. Your employer’s half comes directly from their payroll budget, never from your wages.

This is why self-employed people pay 15.3% in self-employment tax — they are both the employee and the employer, so they cover both halves themselves. As a W-2 worker at your first job, you only pay the employee half.

FICA vs federal income tax — the difference every first-timer misunderstands

Your pay stub has two types of federal taxes and they work completely differently. Most first-time workers assume they are the same thing. They are not.

| Feature | FICA | Federal income tax |

|---|---|---|

| What it funds | Social Security and Medicare programs | General federal government operations |

| Rate | Fixed — always 7.65% | Progressive — 10% to 37% based on income |

| Applied to | Gross wages — before pre-tax deductions | Taxable income — after standard deduction and pre-tax benefits |

| Affected by your W-4? | No — W-4 has zero effect on FICA | Yes — your W-4 controls federal income tax withholding |

| Can you claim exempt? | No — almost never | Yes — if you meet IRS conditions |

| Do you get it back? | No — it is a tax, not a withholding | Possibly — if over-withheld you get a refund in April |

| Employer also pays? | Yes — employer matches 7.65% | No — employer does not match income tax |

The simplest way to think about it: Federal income tax is money you lend to the government for the year — you might get some back as a refund. FICA is money you invest in your future safety net — it does not come back, but it builds your retirement and healthcare benefits.

⚠️ Claiming exempt on your W-4 does not stop FICA

A very common first-job mistake — especially for teenagers. Claiming exempt on your W-4 stops federal income tax withholding, but FICA still comes out of every single check regardless. If you see Social Security and Medicare on your pay stub after claiming exempt, that is correct. Your W-4 has absolutely no power over FICA.

Does FICA come out before or after your 401(k)?

FICA is calculated on your gross wages — the total amount before any pre-tax deductions like a 401(k), health insurance, HSA, or FSA.

This is important to understand: contributing to a 401(k) lowers your federal income tax because it reduces your taxable income. But it does not lower your FICA tax. Your Social Security and Medicare are still calculated on the full gross amount your employer pays you — before any voluntary deductions come out.

What does reduce FICA?

Most pre-tax deductions — like a 401(k) or health insurance — lower your federal income tax but not your FICA. Some employers set up their health insurance or FSA benefits in a special way that also lowers FICA slightly. This depends entirely on how your employer structured the plan and is not common at most first jobs. The standard rule: FICA applies to your full gross wages.

Do you get FICA tax back?

No. FICA is not a withholding that gets reconciled at tax time — it is a tax. It does not appear on your annual tax return as something owed or refundable.

However, you do receive real benefits from it later in life:

Social Security benefits

Every paycheck you pay FICA on builds your Social Security record. In 2026, you earn one credit for every $1,890 in covered wages, up to four credits per year. After 40 lifetime credits — roughly 10 years of work — you qualify for retirement benefits. The more you earn over your career, the higher your eventual monthly payment when you retire.

Medicare coverage

When you turn 65, you become eligible for Medicare — federally funded health insurance. The Medicare taxes you pay throughout your entire working life fund Part A, which covers hospital care. You have been paying into this program since your very first paycheck.

One exception — Social Security overpayment refund

If you work two jobs in the same year and your combined wages from both exceed $184,500, you may have paid more Social Security tax than required. You can claim the excess as a credit on your annual tax return. This only affects the Social Security portion — not Medicare. At typical first-job wage levels, your combined income is unlikely to exceed $184,500, but it is worth knowing for future reference.

Can you avoid paying FICA?

Almost never. FICA applies to virtually every W-2 employee regardless of age, income level, or how you fill out your W-4. A few narrow exceptions exist:

Who may be exempt from FICA:

- Some student workers — college students working part-time at their own university while enrolled at least half-time may be FICA-exempt on those specific earnings only

- Certain nonresident aliens — some visa categories are exempt from FICA withholding

- Some religious group members — members of certain approved religious groups who have filed IRS Form 4029

- Railroad workers — covered by the Railroad Retirement Tax Act instead of FICA

For the vast majority of first-time workers at a regular job — retail, food service, office work, delivery, summer jobs — FICA applies to every paycheck without exception. Age does not matter. A 14-year-old at their first summer job pays FICA the same as a 40-year-old manager.

2026 note — “no tax on tips and overtime” still means FICA applies

The 2026 One Big Beautiful Bill Act introduced a federal income tax deduction for qualified tips and qualified overtime when you file your annual tax return. But this does not make FICA disappear from your paycheck. Social Security and Medicare taxes still apply to regular wages, reported tips, and overtime pay under normal payroll rules — the deduction only affects federal income tax at filing time, not what comes out of each check. If you hear “no tax on tips,” it means a potential deduction on your tax return — not that your employer stops withholding FICA from tip income.

How to plan for FICA on your first paycheck

The simplest way to avoid sticker shock when your first check arrives:

- Estimate your gross pay — hourly rate × hours worked, or annual salary ÷ pay periods

- Subtract 7.65% for FICA — this comes out of every check, always

- Subtract an estimate for federal and state income tax — depends on your income level and W-4

- Subtract any benefits you signed up for — health insurance, 401(k), HSA

- What remains is your estimated take-home pay — budget around this number, not your gross pay

Want to understand when and how often FICA comes out? Read: What Is a Pay Period? →

Frequently Asked Questions About FICA

What is the FICA rate for 2026?

For most employees, the 2026 FICA rate is 7.65% total: 6.2% for Social Security on wages up to $184,500 and 1.45% for Medicare on all wages with no cap. High earners may also owe an additional 0.9% Additional Medicare Tax on wages above $200,000 (single filers) or $250,000 (married filing jointly). These rates are unchanged from 2025. The Social Security wage base increased from $176,100 in 2025 to $184,500 in 2026.

Why is FICA taken from my paycheck?

FICA is taken because federal law requires most employees and employers to contribute to Social Security and Medicare. It is not optional and cannot be removed by your employer or changed through your W-4. The law has required this contribution since 1935 for Social Security and 1966 for Medicare. Every W-2 employee in the United States pays it — including teenagers, part-time workers, and people starting their very first job.

What is FICA on my paycheck?

FICA stands for Federal Insurance Contributions Act. It is a mandatory federal payroll tax that takes 7.65% from every paycheck — 6.2% for Social Security and 1.45% for Medicare. It appears on your pay stub as two separate line items, sometimes labeled OASDI (Social Security) and Medicare or MED. Both are required for almost all employees regardless of age or income.

Why is FICA my biggest deduction?

For many first-time workers — especially teenagers earning below the standard deduction threshold who claim exempt from federal income tax — FICA is the only significant deduction. Because it is a flat 7.65% with no exceptions, it comes out even when federal income tax does not. On a $15/hour first job, FICA might take $45 per week while federal income tax takes nothing. That makes FICA appear larger by comparison — because for many first-timers, it is the only federal tax being withheld.

What is the difference between FICA and federal income tax?

FICA is a flat 7.65% payroll tax that funds Social Security and Medicare — it applies to gross wages, is not affected by your W-4, and does not come back as a refund. Federal income tax is calculated based on your taxable income and filing status — it is affected by your W-4, goes to the general federal budget, and can come back as a refund if you overpaid. Both appear as separate line items on your pay stub.

Does FICA come out before or after 401(k)?

FICA comes out of your gross wages — before pre-tax deductions like a 401(k) are applied. Contributing to a 401(k) lowers your federal income tax because it reduces your taxable income. But Social Security and Medicare are still calculated on your full gross pay. This is one reason why the tax savings from a 401(k) are slightly smaller than people expect — FICA does not shrink along with your federal income tax.

Do I get FICA back on my tax refund?

No. FICA is a tax — not a withholding that gets reconciled at tax time. Federal income tax can come back as a refund if your employer over-withheld. FICA usually does not — except in rare Social Security overpayment cases. The 7.65% taken from each paycheck goes directly into the Social Security and Medicare trust funds. The only partial exception is if you worked two jobs and your combined Social Security withholding exceeded the annual wage base maximum — in that case you can claim the excess as a tax credit.

I am a teenager — do I still pay FICA?

Yes. There is no age exemption for FICA. Whether you are 14 or 64, if you earn W-2 wages, you pay Social Security and Medicare taxes. The only common exception is for students working part-time at their own university while enrolled at least half-time; but a standard part-time or summer job at a restaurant, grocery store, or retail chain is fully subject to FICA regardless of age. For a full breakdown of every tax that comes out of a teenager’s paycheck; not just FICA- see our guide on what taxes teenagers pay on their first paycheck. For exact dollar amounts at common teen wages- $10, $12, and $15 per hour; see our guide on how much minors get taxed on their paycheck.

What if I work two jobs — do I overpay Social Security?

Possibly. Each employer withholds Social Security independently, so if your combined income from both jobs exceeds $184,500 in 2026, you will have overpaid. You can claim the excess Social Security tax as a credit on your annual tax return. You do not get the Medicare portion back — there is no wage cap for Medicare. At typical first-job wage levels, combined income from two jobs is unlikely to exceed $184,500, but it is worth knowing for the future.

What if my parents claim me as a dependent?

Being claimed as a dependent does not exempt you from FICA. It may affect your standard deduction amount for federal income tax purposes — but FICA is completely separate from federal income tax. You still pay Social Security and Medicare on every paycheck regardless of your dependent status. When you file your own taxes, make sure you do not also claim yourself as a dependent if your parents are claiming you.

Does my employer pay FICA too?

Yes. For every dollar of FICA you pay, your employer pays the exact same amount. You pay 7.65% and your employer pays 7.65% — totaling 15.3% of your wages going into Social Security and Medicare. Your employer’s contribution never appears on your pay stub because it is paid separately from their own payroll budget. This is why self-employed workers pay 15.3% self-employment tax — they must cover both halves themselves with no employer to split the cost.

Is FICA the same as Social Security tax?

Not exactly. FICA includes both Social Security (6.2%) and Medicare (1.45%). Social Security tax is just one component of FICA. When people say FICA they usually mean the combined 7.65%. When they say Social Security tax they mean just the 6.2% portion. Both terms refer to the same mandatory federal payroll contribution system and both appear on your pay stub.

The bottom line on FICA

FICA is not a penalty. It is not a mistake. It is a mandatory contribution to Social Security and Medicare that every W-2 employee pays — including you, starting from your very first paycheck.

It takes 7.65% of your gross wages every check. You do not get it back at tax time. But unlike federal income tax, it is building something real — your future retirement income and healthcare coverage.

The best thing you can do as a first-time worker is expect it. Build your budget around your net pay, not your gross pay. And if you want to see the exact FICA amount — and every other deduction — for your specific job, the calculator below does the math in seconds.

Once FICA and the rest of your taxes come out, what’s left is the number that actually matters for budgeting. The 50/30/20 rule for your first paycheck shows exactly how to divide that take-home amount into needs, wants, and savings at $15, $18, and $20 an hour.

See Exactly How Much FICA Takes From Your Check

Enter your hourly rate or salary and see your estimated take-home pay broken down line by line — including the exact Social Security and Medicare amounts — using official 2026 IRS figures.

About the Author

Ashief Mahmood is the Founder and Editor of First Paycheck Guide. He researches and explains first-paycheck topics for U.S. first-time workers using IRS publications, U.S. Department of Labor resources, official employer documentation, payroll sources, and carefully labeled estimates.

Ashief is not a financial advisor, tax professional, payroll provider, lawyer, or employer representative. First Paycheck Guide is an independent educational website.

The information in this article is for educational purposes only and does not constitute tax or financial advice. FICA rates confirmed via IRS Tax Topic 751. Social Security wage base ($184,500 for 2026) confirmed via SSA.gov. Social Security credit eligibility sourced from SSA.gov. Always verify current rates at irs.gov and ssa.gov. Consult a tax professional for advice specific to your situation.