The 50/30/20 Rule for Your First Paycheck (Real Numbers, Not Monthly Guesses)

⚡ The 50/30/20 rule on your first paycheck — quick answer

The 50/30/20 rule divides your after-tax paycheck into 50% for needs, 30% for wants, and 20% for savings or extra debt payments. Start with the net amount deposited into your account, not your hourly rate or gross paycheck. If retirement, HSA, or insurance contributions were already deducted, count those toward the appropriate category instead of ignoring them. On a $1,000 net check with no other deductions, that is $500 needs, $300 wants, and $200 savings.

- Start with net pay — the amount after FICA and taxes, then add back any retirement or insurance deductions and sort them into the right bucket.

- 50% needs — rent share, transport, groceries, phone, minimum debt payments.

- 30% wants — anything not essential: dining out, subscriptions, shopping.

- 20% savings — emergency fund first, then retirement or other goals.

Most articles about the 50/30/20 rule use a $3,500-a-month example. That may be realistic for some new graduates, but it does not help if you are looking at an individual weekly or biweekly deposit, especially when hours, deductions, or your first pay period are irregular.

This guide applies the 50/30/20 rule to your first paycheck using the net pay shown on your own pay stub, with real biweekly examples at common entry-level wages.

Table of Contents

What is the 50/30/20 rule?

The 50/30/20 rule is a simple way to split your paycheck into three categories: 50% for needs, 30% for wants, and 20% for savings or extra debt payments. It was popularized by Elizabeth Warren and Amelia Warren Tyagi in their 2005 book on personal finance, and it has become one of the most common starting points for budgeting because it is easy to remember and easy to apply.

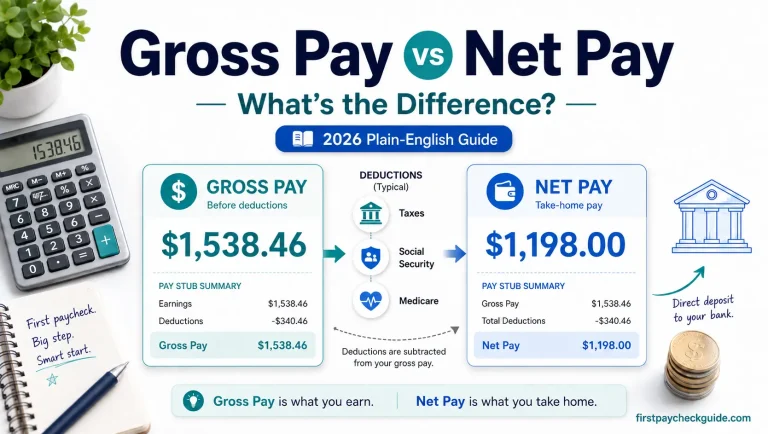

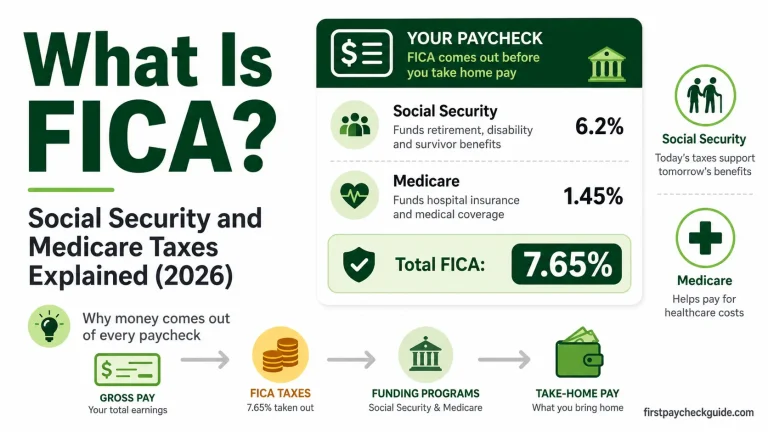

The rule works off your net pay, not your gross pay and not your hourly rate. Net pay is the amount that actually lands in your bank account after federal tax, state tax, and FICA (Social Security and Medicare) are taken out.

The number most guides skip explaining

Almost every 50/30/20 article tells you to use “after-tax income” and then moves on, assuming you already know what that number is. If you are looking at your first pay stub and are not sure which line to use, the number you want is labeled Net Pay or Take-Home Pay, not Gross Pay.

Where the rule comes from

The 50/30/20 rule was popularized by Elizabeth Warren and Amelia Warren Tyagi in their 2005 book, All Your Worth: The Ultimate Lifetime Money Plan. The Consumer Financial Protection Bureau also presents the 50/30/20 framework as a way to divide take-home pay. It was designed to simplify budgeting by removing the need to track dozens of spending categories, which is part of why it remains a popular starting point for people budgeting for the first time.

Is the 50/30/20 rule based on gross or net pay?

Net. The 50/30/20 rule is applied to your take-home pay after federal tax, state tax, and FICA, not your hourly rate, salary, or the gross number on your offer letter. Using gross pay is one of the most common mistakes first-time workers make, because the hourly rate or salary figure is usually the first number you see and the easiest to remember.

| If you budget using | What happens |

|---|---|

| Gross pay ($1,200) | In this example, your budget would be overstated by about 17%. The actual difference may be higher or lower depending on taxes and deductions. |

| After-tax pay (~$1,000) | The correct starting point. Account separately for any retirement, insurance, HSA, or other deductions already taken from the check. |

In this illustration, a $15-an-hour biweekly check shows a gap of roughly $200 between gross and net pay, or more than $400 a month. That gap is large enough to break a budget built on the wrong number, though your actual gap will depend on your state and withholding.

What if my pay stub already shows deductions for retirement or insurance?

If your pay stub already includes a 401(k), health insurance, HSA, or similar deduction, that money has not disappeared. Your 401(k) contribution already counts toward your 20% savings target, and a necessary health insurance premium generally counts toward your 50% needs target. For the most accurate picture, look at your gross pay, subtract only taxes and FICA, and then sort each remaining deduction (retirement, insurance, and so on) into needs or savings rather than ignoring it.

For example, suppose $900 reaches your checking account, while $75 went to your 401(k) and $25 went to health insurance. Your budgeting base is actually $1,000 after taxes: the $900 deposited plus the $100 already assigned through payroll. The $75 counts toward your 20% savings target, and the $25 counts toward your 50% needs target.

Why most 50/30/20 examples do not match a first paycheck

Only know your annual salary? Divide it by 26 to estimate your biweekly gross pay. Your net pay will depend on taxes, your W-4, benefits, and other payroll deductions.

Search for the 50/30/20 rule and most articles use the same kind of example: a smooth $3,500 or $4,000 monthly take-home figure. That may be realistic for some new graduates, but it does not help if you are looking at an individual weekly or biweekly deposit, especially when hours, deductions, or your first pay period are irregular.

| What most guides use | What a first paycheck may look like |

|---|---|

| $3,500–$5,000 per month after tax | $700–$1,300 every two weeks after tax |

| Monthly budgeting examples | Weekly or biweekly deposits for many hourly and entry-level workers |

| Stable salaried-income assumptions | Hourly pay, variable shifts, overtime, or a partial first pay period |

This guide skips the generic monthly example and goes straight to real biweekly paycheck amounts at common entry-level wages, using the net pay shown on your own pay stub.

How to use the 50/30/20 rule on your first paycheck

These examples use a standard 80-hour biweekly schedule and assume approximately 17% of gross pay is withheld for FICA, federal income tax, and an illustrative state income tax amount, leaving roughly 83% as net pay. Your actual take-home pay may be higher or lower depending on your state, W-4, filing status, benefits, and retirement contributions.

These figures are illustrative estimates only. Replace the estimated net amount with the net pay shown on your own pay stub for an accurate budget.

$15 an hour — biweekly paycheck

| Item | Amount |

|---|---|

| Gross pay (80 hours) | $1,200.00 |

| Estimated net pay | ~$1,000.00 |

| 50% Needs | ~$500.00 |

| 30% Wants | ~$300.00 |

| 20% Savings | ~$200.00 |

$18 an hour — biweekly paycheck

| Item | Amount |

|---|---|

| Gross pay (80 hours) | $1,440.00 |

| Estimated net pay | ~$1,190.00 |

| 50% Needs | ~$595.00 |

| 30% Wants | ~$357.00 |

| 20% Savings | ~$238.00 |

$20 an hour — biweekly paycheck

| Item | Amount |

|---|---|

| Gross pay (80 hours) | $1,600.00 |

| Estimated net pay | ~$1,320.00 |

| 50% Needs | ~$660.00 |

| 30% Wants | ~$396.00 |

| 20% Savings | ~$264.00 |

Where the net pay estimate comes from

These figures assume roughly 17% in combined FICA, federal, and state tax withholding for a single filer with no extra benefit deductions. Your actual net pay depends on your state, your W-4 settings, and any benefit deductions like health insurance or a 401(k) contribution, which would lower the deposit further but count toward needs or savings as explained above. For a more personalized estimate, use the gross-to-net calculator below with your hourly rate and hours.

| If your net paycheck is… | 50% Needs | 30% Wants | 20% Savings |

|---|---|---|---|

| $600 | $300 | $180 | $120 |

| $800 | $400 | $240 | $160 |

| $900 | $450 | $270 | $180 |

| $1,000 | $500 | $300 | $200 |

| $1,200 | $600 | $360 | $240 |

| $1,400 | $700 | $420 | $280 |

Find the row closest to your net pay, or use the calculator below for your exact number first.

Calculate Your Own 50/30/20 Split

Enter your hourly rate and hours to estimate your take-home pay, then apply the percentages above to your real number.

What counts as needs, wants, and savings on a first paycheck

The categories are simple in theory, but the actual line items look different for an 18 to 22 year old than they do for someone with a mortgage and kids. Here is what each bucket realistically includes on a first job.

50% Needs

Rent or rent share, groceries, transportation (gas, bus pass, car payment), phone bill, minimum payments on any existing debt, and any insurance you are responsible for. If you are still on a parent’s health insurance or family phone plan, your needs bucket may be smaller than the standard 50%.

Minimum required debt payments belong here. Any amount paid above the minimum counts toward the 20% savings and extra-debt category instead.

30% Wants

Dining out, streaming subscriptions, clothing beyond the basics, entertainment, hobbies, and anything you are buying because you want it, not because you need it. This is often the easiest bucket to overspend, not because the money is wrong, but because the purchases are individually small and easy to lose track of.

If your needs bucket is smaller than 50%

Many first-job workers in their late teens or early twenties are still on a parent’s health insurance and phone plan, or are living at home rent-free. If that is your situation, your actual needs may only take up 25 to 35% of your paycheck instead of the standard 50%. Rather than letting that extra money drift into wants, consider shifting it into the 20% savings bucket while your expenses are this low. This stage does not last, and the extra savings window is easy to miss until it has already closed.

20% Savings — where it actually goes first

| Priority order | Where the money goes | Why first |

|---|---|---|

| 1 | Starter emergency fund ($500–$1,000) | Covers a car repair or unexpected expense without going into debt |

| 2 | Any employer 401(k) match | Additional compensation you only get if you contribute. Contribute at least enough to get the full match. |

| 3 | High-interest debt (credit cards) | Interest charges typically outpace what you would earn from savings or investing |

| 4 | Larger emergency fund | Builds protection against job loss and larger unexpected expenses |

| 5 | Roth IRA or additional retirement savings | Supports long-term retirement growth; qualified Roth IRA withdrawals can be tax-free |

This is a common starting order, not a universal rule. Your priorities may differ based on your situation.

The biweekly paycheck problem most budgeting guides ignore

Most 50/30/20 articles assume a monthly paycheck. If you are paid biweekly, you are actually getting 26 paychecks a year, not 24. That means twice a year, you get a third paycheck in a month where you would normally only expect two.

The three-paycheck month opportunity

A three-paycheck month creates a useful cash-flow opportunity, but that third check is still part of your normal annual income, not extra money. Before sending it entirely to savings, set aside anything needed for irregular expenses coming up, like a car repair, holiday spending, or an annual insurance premium. Whatever is left after that is a strong candidate for extra savings.

When the 50/30/20 rule does not fit your first paycheck

The 50/30/20 rule is a guideline, not a law. A few common first-job situations where the standard split needs adjusting:

| Situation | Adjusted split | Why |

|---|---|---|

| High cost-of-living city, rent alone exceeds 50% | 60/30/10 or 65/25/10 temporarily | Needs can cost more than half your paycheck in some areas |

| Living at home, minimal expenses | 20/30/50 or similar | Take advantage of low needs while it lasts |

| Aggressively paying off debt | 50/20/30 | Shift wants money toward extra debt payments |

| First paycheck is a partial period | Cover essentials first, save what you can, apply the full split starting with your next full check | A short first check is not representative of your normal pay |

Example: when essential expenses exceed 50%

Suppose you take home about $1,190 every two weeks and pay $1,300 a month for rent and utilities. That works out to roughly $600 from each biweekly paycheck for housing alone. After adding groceries, transportation, insurance, and minimum debt payments, your total needs could easily exceed 50% of the check. In that situation, a temporarily adjusted split such as 60/25/15 may be more realistic: about $714 for needs, $298 for wants, and $179 for savings. The goal is not a perfect 50/30/20 every check. It is keeping savings above zero while your income or living situation improves.

If the standard split still feels too tight

You can temporarily use a different split, such as 70/20/10 or 60/30/10, and move closer to 50/30/20 as your income or circumstances improve. Even in a difficult month, try to keep a small amount, such as $20 or $25, going toward savings. When you are just starting out, building the habit can matter more than reaching the full 20% immediately.

How to set up the 50/30/20 split on your first paycheck

- Find your net pay on your pay stub, not your gross pay or hourly rate.

- Multiply that number by 0.50, 0.30, and 0.20 to get your three target amounts.

- Ask HR for a split direct deposit form if your employer offers one.

- Open a separate savings account, ideally a high-yield savings account, away from your everyday checking account.

- Set your 20% savings target to auto-deposit there every payday.

- Track needs and wants spending for one full pay cycle to see where you actually land versus the target.

Frequently asked questions about the 50/30/20 rule on a first paycheck

Do I use my salary or my actual paycheck amount for the 50/30/20 rule?

Use your actual net pay from your pay stub, not your salary or hourly rate. If you are paid biweekly, apply the rule to each individual paycheck rather than trying to estimate a monthly average, especially in your first few months when your schedule may not be fully predictable.

Is the 50/30/20 rule based on gross or net income?

Net income. The rule is meant to apply to the money you actually have available to spend, which is your take-home pay after federal tax, state tax, and FICA are withheld. Using gross pay will overestimate how much you actually have for needs, wants, and savings.

What if my first paycheck is smaller than expected?

A first paycheck is often a partial pay period, covering fewer days than a normal check. Use that first check to cover expenses due before your next payday and save a small amount if you can. Begin applying the full 50/30/20 split starting with your second, full paycheck, which will better represent your normal pay.

How much of my first paycheck should I save?

20% is the standard target under the 50/30/20 rule, but if your needs are unusually low, for example if you are living at home or still on a parent’s insurance, you may be able to save more. If your needs are unusually high, even 10% is a reasonable starting point as long as you are saving something consistently.

What counts as a need if I still live with my parents?

If you live at home, your needs bucket may only include a few items: transportation, your phone bill if you cover it, groceries or a household contribution if asked, and any debt payments. Your needs percentage is often well below the standard 50% in this situation, which is a good opportunity to increase your savings percentage instead.

Should retirement contributions count as savings or needs?

Retirement contributions, including 401(k) and Roth IRA contributions, count toward the 20% savings bucket. If your employer offers a 401(k) match, prioritize contributing at least enough to get the full match before allocating savings elsewhere, since an employer match is additional compensation you generally only receive when you contribute under the plan’s rules.

Is the 50/30/20 rule realistic on minimum wage or entry-level pay?

It can be tight, especially in a high cost-of-living area. If your needs exceed 50% of your paycheck, a temporary adjusted split such as 60/30/10 may be more realistic than forcing the standard percentages. The goal is to keep some amount flowing to savings consistently, even if it is less than 20% at first.

Do I budget monthly or by paycheck if I get paid biweekly?

Budgeting by paycheck is usually simpler when you are biweekly, especially early on. Apply the 50/30/20 split to each individual check rather than trying to average two checks into a monthly total. Keep in mind that biweekly pay results in 26 paychecks a year, which means two months each year include a third paycheck.

The bottom line on 50/30/20 for your first paycheck

The 50/30/20 rule works the same way for a first job as it does for any other income, but most examples online use monthly figures that do not match a real entry-level paycheck. Start with your actual net pay, not a generic monthly estimate.

- Use net pay, not gross pay. The number on your pay stub, not your hourly rate or salary.

- Apply it per paycheck if you are biweekly. Do not wait to average two checks together.

- Adjust for your situation. Living at home or still on a parent’s insurance can mean a smaller needs bucket and a bigger savings opportunity.

Estimate Your Net Pay Before You Budget

Enter your hourly rate and hours to estimate your take-home pay, then apply the 50/30/20 split to that amount.

The information in this article is for educational purposes only and does not constitute financial advice. Net pay estimates are approximate and will vary by state, W-4 settings, and benefit deductions. For your actual take-home pay, review your pay stub. You can use the calculator linked above for an estimate before your paycheck arrives. Consult a financial professional for advice specific to your situation.